Reviewed against Gazette Notifications G.S.R. 525(E) [EPF], G.S.R. 527(E) [EPS], and G.S.R. 526(E) [EDLI], all dated June 29, 2026, Ministry of Labour and Employment by Kustodian Research Team

Quick Answer

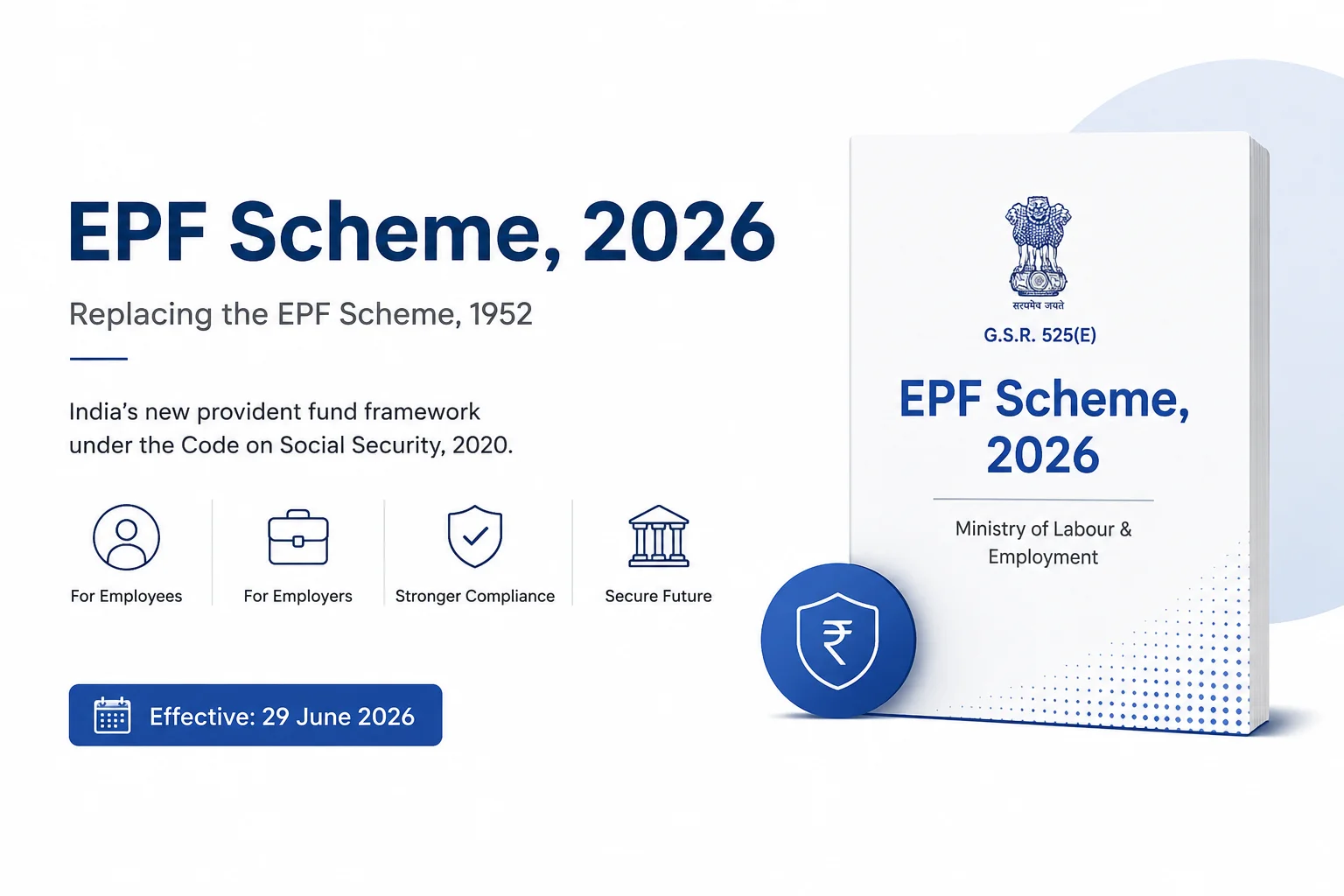

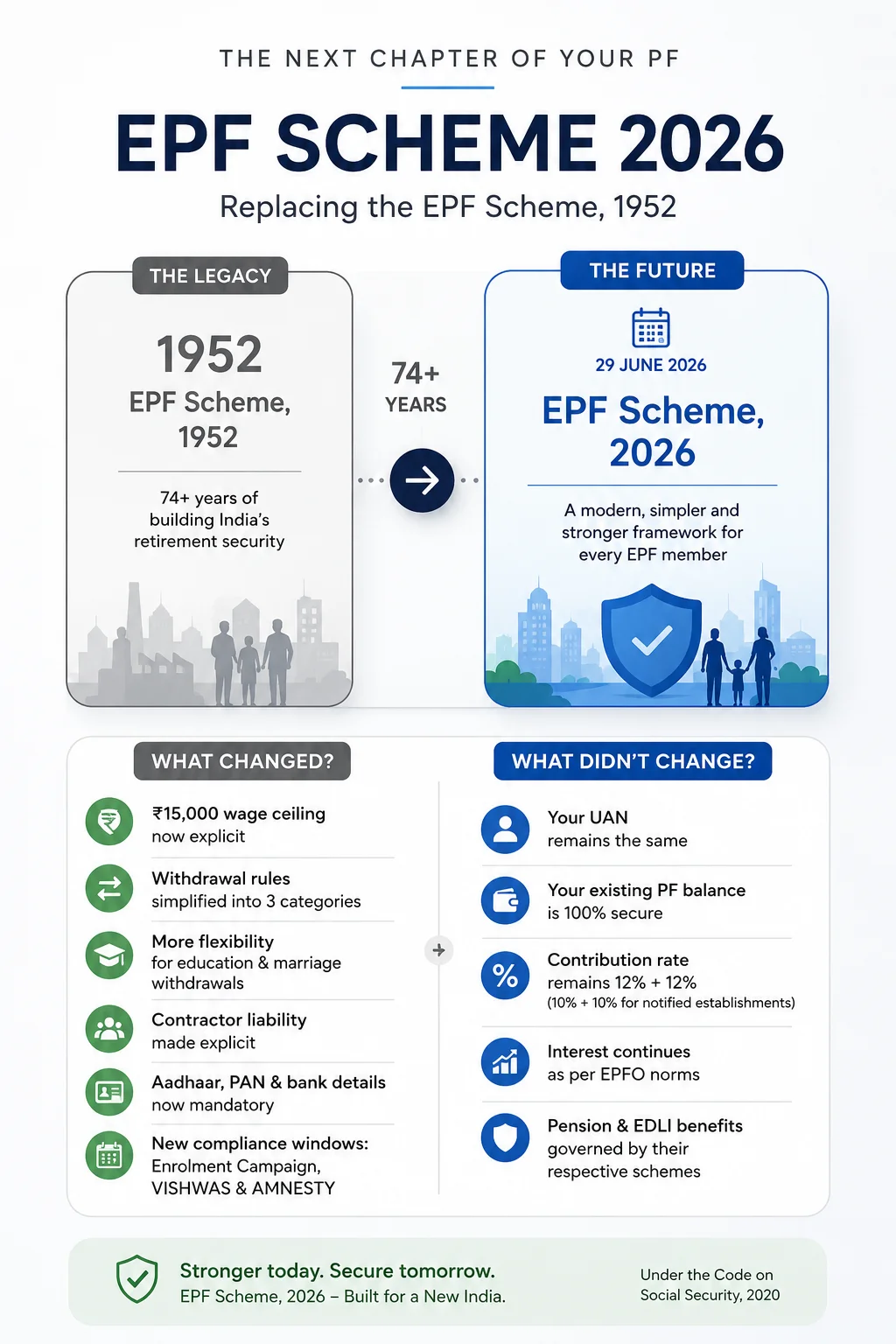

The Employees' Provident Fund Scheme, 2026 (G.S.R. 525(E)) is India's new legal framework for EPF, notified June 29, 2026, under the Code on Social Security, 2020, replacing the EPF Scheme, 1952. Two companion schemes were notified the same day — the Employees' Pension Scheme, 2026 (G.S.R. 527(E)) and the EDLI Scheme, 2026 (G.S.R. 526(E)) — each covered on its own page, linked below. For most employees, contributions, UAN, and existing balances carry over automatically, with no action required. What's actually new: the ₹15,000 mandatory-contribution ceiling is now spelled out explicitly rather than implied, partial withdrawals are simpler but frequency-capped, and three time-bound compliance windows — for employees who were never formally enrolled, disputed damages, and informal PF trusts — are open only until later this year.

EPF Scheme 2026 at a Glance

| Item | Detail |

|---|---|

| Notification | G.S.R. 525(E), Ministry of Labour and Employment |

| Companion notifications | EPS 2026 — G.S.R. 527(E); EDLI 2026 — G.S.R. 526(E) (same date) |

| Effective from | June 29, 2026 |

| Replaces | EPF Scheme, 1952 |

| Legal basis | Section 15(1)(a), Code on Social Security, 2020 |

| Contribution rate | 12% employee + 12% employer (10%+10% for notified establishments) |

| Mandatory contribution cap | ₹1,800/month each — 12% of the ₹15,000 wage ceiling |

| FY 2025-26 interest rate | 8.25% p.a. |

| Withdrawal categories | 13 provisions consolidated into 3 |

| Compliance windows open | Enrolment Campaign (to Oct 31, 2026); VISHWAS & AMNESTY (6 months from notification, extendable by 6 more) |

Don't Confuse These Similar Terms

| Term | What It Is |

|---|---|

| EPF Scheme, 2026 (G.S.R. 525(E)) | Governs EPF contributions, accounts, and withdrawals. This page. |

| EPF Scheme, 1952 | Superseded, except for actions already completed under it. |

| EPS 2026 (G.S.R. 527(E)) | Separate pension scheme; replaces EPS 1995 and the Employees' Family Pension Scheme, 1971. → Read the EPS 2026 guide |

| EDLI Scheme, 2026 (G.S.R. 526(E)) | Separate death-in-service insurance benefit. → Read the EDLI 2026 guide |

| Code on Social Security, 2020 | The parent law under which EPF, EePS, and EDLI are all notified. |

| Enrolment Campaign / VISHWAS / AMNESTY, 2026 | Three time-bound compliance-relief measures introduced by this same EPF notification — not separate schemes. |

Takeaway: This page governs your PF account specifically. Pension and insurance are separate, related schemes — not replaced or absorbed by this one.

Why This Changed Now

The EPF Scheme, 2026, isn't a standalone reform — it's the provident-fund installment of a longer rollout. The Code on Social Security, 2020, along with India's three other labour codes, came into force on November 21, 2025, replacing nine older labour statutes in one stroke. Because pension and insurance rules couldn't be rewritten overnight, the Code built in a one-year transition — until November 20, 2026 — during which the old EPS and EDLI schemes stayed in force while a replacement framework was drafted.

The procedural rules needed to actually operate the Code — the Social Security Code (Central) Rules, 2026 — were notified on May 8, 2026. The EPF, EPS, and EDLI Schemes, 2026, followed on June 29, 2026, issued under Section 15 of the Code. That's roughly five months ahead of the November deadline: this notification is the provident-fund leg of the transition arriving early, not a change employees or employers asked for or need to react to defensively.

What's New in the EPF Scheme, 2026?

| Change | Detail | Who It Matters To |

|---|---|---|

| Wage ceiling is now explicit | Mandatory 12% applies only up to ₹15,000 in wages (₹1,800/month each side). Anything contributed above that is formally voluntary — either side can reduce or stop it unilaterally. This codifies a rule that technically existed since 1952; what's new is that it's now written into the Scheme itself, and the exit from it is explicitly unilateral. | Employees earning above ₹15,000 basic; payroll teams |

| Withdrawals simplified, but frequency-capped | 13 overlapping provisions merged into 3 categories: Essential Needs (illness, education, marriage), Housing Needs, and Special Circumstances. Education withdrawals: up to 10 times over a career (up from a combined limit of 3 shared with marriage). Marriage withdrawals: up to 5 times. A 25% minimum-balance rule applies across all partial withdrawals, available after 12 months of membership. | Anyone planning a partial withdrawal |

| Exit before 12 months | Members who leave a job before completing 12 months can still withdraw up to 100% of their eligible balance — capped at two such withdrawals per financial year. | Employees between jobs early in a roleThe |

| EPS pension withdrawal wait has been extended | The wait to withdraw your EPS pension corpus after leaving a job — with no new EPF-covered employer — moves from 2 months to 36 months. Rejoin an EPF-covered employer within that window, and your pension service continues instead of requiring a withdrawal. | Anyone recently between jobs |

| Contractor liability made explicit | Where contract workers' PF is routed through a contractor, the principal employer is now expressly, ultimately liable if the contractor defaults — even where the contractor is the one remitting. | Employers using contract labour |

| Digital mandates written into law | Aadhaar-linked UAN, PAN, and Aadhaar-seeded bank details are now statutory filing requirements, not just portal conveniences; consolidated returns must be filed within 15 days of the month close. | Employees with unlinked Aadhaar; HR/payroll teams |

| Emergency deferral power | The Central Government may defer or reduce both employer and employee contributions for up to 3 months during a pandemic, epidemic, or national disaster. | A contingency provision — not currently active |

| Exempted PF trust interest cap | Company-run PF trusts (exempted establishments) can no longer declare an annual interest rate more than 200 basis points above the EPFO-declared rate. | Employees at companies with private PF trusts, and employers running them |

| Three compliance windows opened | Enrolment Campaign, VISHWAS, and AMNESTY — each solves a different, specific compliance gap, each time-bound. | Employers with historical gaps; long-tenured employees never formally enrolled |

What This Means in Practice

Anjali earns a basic salary of ₹40,000/month. Her mandatory PF contribution stays capped at ₹1,800/month (12% of ₹15,000), matched by her employer. If her employer currently contributes on her full ₹40,000 basic — common at some companies — that extra ₹3,000/month is now explicitly voluntary on both sides; either can reduce or stop it going forward, without notice periods or statutory objection. Her UAN, balance, and contribution history are untouched either way.

Quick check: if your monthly PF deduction is exactly ₹1,800 despite a higher basic salary, you're on the statutory ceiling track. A higher deduction means you're on the voluntary track — worth confirming with payroll, since it's now explicitly easier for either side to change.

What Has NOT Changed

| Topic | Status |

|---|---|

| Existing EPF balance, UAN | Continue automatically — no re-enrolment, no new UAN |

| Contribution rate | Still 12%+12% (10%+10% for notified establishments) |

| FY 2025-26 interest rate | 8.25% p.a. |

| EPS pension formula | Pensionable Salary × Pensionable Service ÷ 70 |

| EPS contribution split | 8.33% employer + 1.16% Central Government, unchanged |

| Tax treatment, nomination rules | Unchanged |

| Claims filed under the 1952 Scheme | Continue to their conclusion; only future actions fall under the 2026 Scheme |

What the Scheme Does NOT Fix — Kustodian's Two-Layer Framework

Think of your EPF account in two layers. Layer 1 is the legal framework — contribution rates, withdrawal rules, and scheme structure. This is what the 2026 notification updates. Layer 2 is your personal record — KYC, service history, nomination, and employer data. The 2026 Scheme does not touch Layer 2, and Layer 2 is what actually determines whether your next claim goes smoothly.

| Existing Problem | Fixed by 2026 Scheme? | What to Do |

|---|---|---|

| Missing service history | No | Verify service history |

| Wrong Date of Exit | No | Request employer correction |

| Aadhaar/KYC mismatch | No, though Aadhaar linking is now mandatory | Complete KYC verification |

| Multiple UANs | No | Merge duplicate UANs |

| Missing EPS contributions | No | Review EPS eligibility |

| Missing nomination | No | Update nomination |

| Unverified bank account | No | Verify bank details |

Two employees at the same company, on the same salary, can have completely different claim experiences — the difference is almost always Layer 2, not the law.

→ Run a Kustodian EPF Health Check to find out which of these apply to you

Common Misconceptions About the EPF Scheme, 2026

"My take-home pay will drop." Not from this notification alone. Contribution rates are unchanged. Take-home pay only shifts if your employer actively restructures payroll around the now-explicit ₹15,000 ceiling — and for some employees on the voluntary track today, that shift would raise take-home pay, not lower it.

"I need to re-register or get a new UAN." No. This is the single most searched misconception about this notification, and it's simply false — see What Hasn't Changed above.

"This means EPFO gave me a pension hike." No. The EPS 2026 pension formula, contribution split, and wage ceiling are all carried forward unchanged. Nothing in this notification increases the pension amount you'll eventually receive.

"Voluntary contributions above ₹15,000 are no longer allowed." The opposite: they're formally recognized and permitted, just correctly labeled as voluntary rather than treated as an unstated obligation. You, or your employer, can now adjust or stop them without ambiguity about whether that's allowed.

"My pending claim under the old 1952 Scheme is now void." No. The 2026 Scheme explicitly preserves actions already taken under the 1952 Scheme. A claim filed before June 29, 2026, continues to its conclusion under the rules it was filed under.

The Three 2026 Compliance Windows

The same June 29 notification also opened three time-bound relief measures, introduced as part of the EPF Scheme, 2026 itself — not as separate schemes. Treat these as a co-equal third pillar of the notification, alongside the wage-ceiling and withdrawal changes above.

| Employees' Enrolment Campaign, 2026 | VISHWAS, 2026 | AMNESTY, 2026 | |

|---|---|---|---|

| Fixes | Employees who should have been enrolled in EPF but never were | Disputed or pending damages proceedings | Company-run PF trusts operating without formal exemption approval |

| Who it's for | Employers, on behalf of employees who joined between April 1, 2009, and March 31, 2026, and remain employed on the declaration date | Employers with damage disputes tied to defaults from before June 14, 2024 | Employers running an informal PF trust — even one already recognized under the Income Tax Act, 1961 |

| Deadline | Open until October 31, 2026 | 6 months from notification, extendable by 6 more | 6 months from notification, extendable by 6 more |

| What it waives | Employee-side contributions for the unenrolled period, where never deducted; damages for eligible defaults (July 2009–March 2026) capped at ₹100 | Reduces or settles disputed damage amounts | Retrospective exemption recognition; waives certain employee-strength and corpus conditions |

| The employer still owes | Employer's own contributions, plus interest and administrative charges, for the declared period | — | Ongoing compliance, audits, and any surcharge from investment-pattern deviations |

Which one applies to you or your company?

- An employee who suspects they were never formally enrolled despite years of service → the employer needs the Enrolment Campaign.

- An employer with a damages notice or dispute from before mid-2024 → VISHWAS.

- An employer running a private PF trust that was never formally exempted → AMNESTY.

→ Talk to a Kustodian compliance specialist if you're navigating any of these three windows — all close well before the Code's own November 2026 transition deadline.

Does This Affect You?

| You Are | Impact | Recommended Action |

|---|---|---|

| Existing employee | Minimal — confirm your records before your next claim | Check your EPF records |

| Employee earning above ₹15,000, new job | Ask payroll whether contributions run on full basic or the ₹15,000 ceiling | First-time EPF guide |

| Anyone recently between jobs | Your EPS withdrawal wait just moved from 2 months to 36 | EPS 2026 guide |

| Employer | Review payroll against the wage-ceiling, contractor-liability, and digital-filing rules | Employer compliance guide |

| Employer with unenrolled staff or pending disputes | One of the three windows above is open now — check eligibility before it closes | Talk to a specialist |

| Legal heir/nominee | The claim process itself is unchanged | EPF death claim guide |

Before Your Next EPF Claim

☐ Aadhaar linked to UAN · ☐ Nomination updated · ☐ No duplicate UANs · ☐ Date of Exit correct · ☐ If you left a job recently, confirm whether you're inside the new 36-month EPS withdrawal wait

→ Run the full Kustodian EPF Health Check for a complete records review

Official Notifications

| Scheme | Notification No. | Date | Supersedes |

|---|---|---|---|

| EPF Scheme, 2026 | G.S.R. 525(E) | June 29, 2026 | EPF Scheme, 1952 |

| Employees' Pension Scheme, 2026 | G.S.R. 527(E) | June 29, 2026 | EPS 1995 & Employees' Family Pension Scheme, 1971 |

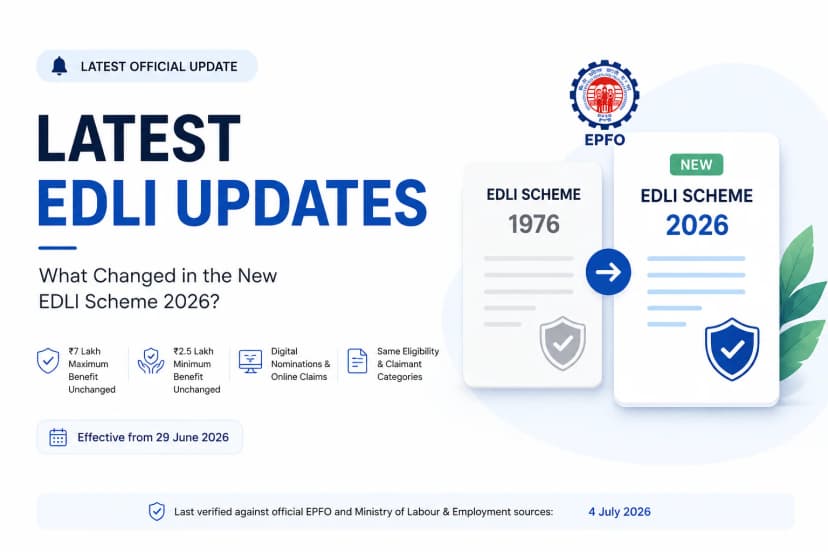

| EDLI Scheme, 2026 | G.S.R. 526(E) | June 29, 2026 | EDLI Scheme, 1976 |

Issued under Section 15, Code on Social Security, 2020 · Ministry of Labour and Employment, Government of India. Official source: e-Gazette of India (egazette.gov.in) and the Ministry of Labour & Employment website (labour.gov.in) — search the G.S.R. number for the exact notification PDF.

Kustodian's interpretation, in plain English: the Scheme replaces the legal shell governing EPF, keeps contribution rates and your account exactly as they were, spells out the ₹15,000 wage-ceiling rule more explicitly than before, simplifies and caps withdrawal frequency, adds a pandemic-contingency deferral power nobody expects to need soon, and opens three compliance windows that close well before most employees would ever notice them. It does not touch your personal records — that responsibility stays with you, your employer, and EPFO.

Continue Your EPF Journey

EPF Scheme, 2026

│

┌───────────────────┼────────────────────┐

Understand the Family Manage Your Account Resolve Problems

│ │ │

EPS 2026 guide UAN Guide EPF Claim Rejected

EDLI 2026 guide Nomination Missing Service History

EPF Health Check KYC Updates Multiple UANs

Employer Compliance Bank Verification Enrolment/VISHWAS/AMNESTY

Frequently Asked Questions

Does the EPF Scheme, 2026, cut my take-home pay?

No — see Common Misconceptions above.

What happens to the Voluntary Provident Fund (VPF) I'm already running?

VPF continues under the same voluntary-contribution logic the Scheme now makes explicit. Nothing about your existing VPF instructions changes automatically.

Is enrolment under the 2026 Scheme optional for me?

No. Coverage remains mandatory the same way it always was, based on your establishment and wage. The Enrolment Campaign exists for employees who should have been covered in the past but weren't — it doesn't make future coverage optional.

I resigned last month, and I'm job-hunting — does the 36-month EPS wait apply to me right now?

Yes, if you have no new EPF-covered employer by the time you'd otherwise apply. Join an EPF-covered employer before then, and your pension account continues instead of needing a withdrawal.

Do employers need to take action beyond the three compliance windows?

Yes — particularly Aadhaar-linked UAN compliance, the 15-day consolidated-return filing requirement, and payroll templates that still assume PF is deducted on full basic salary rather than the explicit ₹15,000 ceiling.

Need Help With Your Own EPF Records?

The law is settled; the details are online. Whether your own account is claim-ready is the part actually worth checking.

→ Run Your EPF Health Check — a records review before you need one