Notification date: 29 June 2026 · Last verified: 2 July 2026

Prepared by: Kustodian — we've helped 9,000+ Indian families recover unclaimed EPF, pension, and insurance assets.

The Ministry of Labour & Employment notified the Employees' Pension Scheme (EPS), 2026 on 29 June 2026, replacing EPS-95 and the Employees' Family Pension Scheme, 1971 (FPS-71) under the Code on Social Security, 2020. Existing membership, core contribution structure, and existing pension entitlements continue, while the notification introduces important administrative and procedural changes — details below.

At a Glance

| Question | Answer |

|---|---|

| Is EPS-95 abolished? | No — replaced as the legal framework. Existing pensions and memberships continue without interruption. |

| Do I need to re-register or reapply? | No. |

| Does my pension amount change? | No — same formula, same ₹1,000 minimum. |

| Do contributions change? | No — 8.33% employer as before. Higher-pension members follow the existing post-Supreme Court contribution framework, now with firmer statutory footing. |

| What actually changed? | Claim settlement deadlines, delay accountability, statutory basis for higher pension, and fund governance. |

| Does the date matter to me? | Only if you're a new joiner. EPS 2026 applies to employees becoming members on or after 29 June 2026; existing members transition automatically under the old accrual, no action needed. |

Why Was EPS 2026 Introduced?

EPS 2026 exists to bring India's statutory employee pension scheme under the Code on Social Security, 2020, consolidating two separate legal instruments — EPS-95 and FPS-71 — into a single notified scheme. It was notified alongside the EPF Scheme, 2026, and EDLI Scheme, 2026, the same week, as part of the broader labour-code rollout.

This is a legal consolidation and governance upgrade, not a pension redesign. The formula, eligibility, and contribution structure stay in place; what changes is how the scheme is administered and enforced — accountability, timelines, and fund governance, covered below.

What Changed

1. Claim settlement now has a legal deadline — and a financial penalty for missing it

EPFO must settle a complete pension claim within 20 days of receiving it. If documents are missing, the applicant must be told what's missing within that same 20-day window — no more indefinite silence.

If a valid claim is delayed without sufficient reason, EPFO owes the claimant 12% annual interest on the delayed amount — a real financial cost for unjustified delay, not just a procedural target.

Why this matters: Anyone with a pending or future pension claim. This is the most concrete, enforceable change in the entire notification.

2. A higher pension gets a statutory home inside the scheme itself

Following the Supreme Court's ruling on higher pension, EPS 2026 formally incorporates the higher-pension framework into the scheme rather than leaving it as a standalone circular-driven process. For eligible members, the scheme carries forward the existing contribution framework notified after the Supreme Court judgment, now with firmer statutory backing rather than a fresh set of numbers.

What this doesn't do: make every member eligible, or retroactively raise anyone's existing pension. Eligibility and the application process EPFO already put in place after the Supreme Court judgment are unchanged — EPS 2026 just gives that process a firmer legal footing.

3. Family pension: same beneficiaries, one newly codified number

Coverage is unchanged — spouse, children, orphans, disabled children, nominees, and dependent parents remain eligible, where applicable. One specific figure is now codified: where there's no surviving spouse, but children survive, they receive an orphan pension equal to 75% of the widow pension.

Why this matters: Family members relying on survivor benefits — worth checking nominee records against this.

4. Fund governance and investment rules are tightened

Pension assets remain invested in the Central government's Public Account. Government contributions made from 1 April 2026 onward carry an assured minimum interest rate of 8.5%. Separately, the scheme introduces stricter governance for exempted trusts — mandatory audits, electronic accounting, and compliance timelines — mainly relevant to employers who run their own PF trusts rather than depositing with EPFO directly.

Why this matters: Members indirectly, through fund stability; exempted-trust employers directly, through new compliance obligations.

What Hasn't Changed

Despite the new legal framework, most pension rules remain exactly the same for existing members.

| Feature | Status |

|---|---|

| Pension formula (Pensionable Salary × Service ÷ 70) | Unchanged |

| Minimum qualifying service (10 years) | Unchanged |

| Minimum monthly pension (₹1,000) | Unchanged |

| Employer/employee contribution rates | Unchanged |

| Existing pensioners | Continue without interruption |

| Existing EPF/EPS membership | Continues automatically, no re-registration |

| UAN | No change |

EPS-95 vs EPS-2026

The table below compares the previous pension framework with the newly notified scheme to help identify what has actually changed.

| Feature | EPS-95 | EPS-2026 |

|---|---|---|

| Legal basis | EPF & MP Act, 1952 | Code on Social Security, 2020 |

| Claim settlement timeline | No statutory deadline | 20 days, with a mandatory deficiency notice |

| Delay penalty | Not codified | 12% annual interest on unjustified delays |

| Higher pension | Governed by post-judgment circulars | Incorporated directly into the scheme |

| Family/orphan pension | Same beneficiary categories | Same categories; orphan pension formally set at 75% of the widow pension |

| Fund investment | Public Account | Public Account: new contributions carry an assured 8.5% minimum interest from the central government to EPFO |

| Exempted trust governance | Lighter compliance regime | Mandatory audits, electronic accounting, stricter reporting |

Should You Do Anything?

Most EPF members do not need to take immediate action. Your next step depends on your current situation.

| Situation | Action |

|---|---|

| Existing pensioner | Nothing — payments continue as before |

| Existing EPF/EPS member | No action required; worth checking records (see below) |

| New employee joining after 29 June 2026 | Normal enrollment — no special steps |

| Pending pension claim | Verify your documentation is complete to start the 20-day clock |

| Higher pension applicant | Continue the existing EPFO process — this notification doesn't change it |

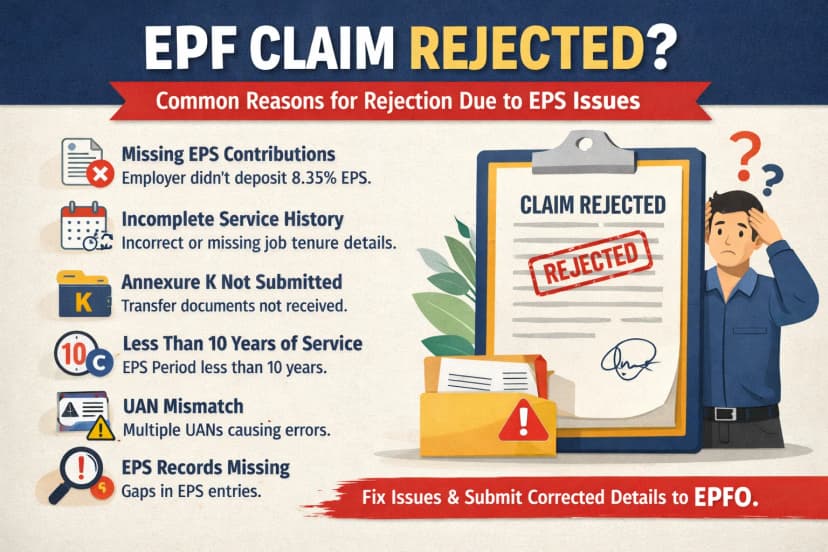

Why Pension Claims Actually Get Delayed {#delays}

None of the above fixes a claim that's stuck because of bad records. Across the 9,000+ EPF and pension cases Kustodian has worked, the most common cause of delay isn't a rule change — it's a member record issue.

| Common issue | Why it matters |

|---|---|

| Incorrect date of joining or exit | Directly affects pensionable service calculation |

| Missing or incorrect service history | Can reduce or interrupt eligibility |

| Aadhaar/PAN mismatch | Delays verification |

| Name or date-of-birth mismatch | Triggers additional manual verification |

| Missing transfer records from a previous employer | Prior service may not reflect correctly |

| Outdated nominee details | Complicates family pension claims specifically |

The 20-day rule only starts the clock once your documentation is complete. If your records have any of the above issues, EPS 2026's new timeline doesn't help you — verifying your EPFO details before you file is still the highest-leverage thing you can do.

If your claim is already stalled over a mismatch like this, Kustodian can audit and correct your EPFO profile before you file.

Common Misconceptions

| Myth | Reality |

|---|---|

| EPS-95 has been abolished | No — replaced as the legal framework; existing entitlements continue |

| Everyone gets a higher pension now | No |

| I need to register again | No |

| I need a new UAN | No |

| The minimum pension has increased to ₹7,500 | No — that's a separate, unconfirmed Budget 2026 proposal, unrelated to this notification |

| This changes retirement age or eligibility rules | No |

FAQ

What is EPS 2026?

The pension scheme is notified under the Code on Social Security, 2020, replacing EPS-95 and FPS-71 while continuing the existing pension framework for eligible employees.

Do I need to apply again?

No.

Will my pension increase?

No.

Does this affect higher pension applications?

It gives the existing higher-pension framework firmer legal standing; it doesn't change who's eligible.

What's the new claim settlement timeline?

20 days, with a 12% interest penalty for unjustified delays.

Should I do anything right now?

Most members don't need to take immediate action. It's a good moment to check your service history, KYC, and nominee details — see Why Claims Get Delayed.

Related Questions

Is EPS different from EPF?

Yes. EPF is your provident fund savings account; EPS is a separate pension fund built from part of the employer's contribution (8.33%, more for higher-pension members under the post-Supreme Court framework). They're administered together but paid out differently — EPF as a lump sum, EPS as a monthly pension.

Can EPS be withdrawn as a lump sum?

Only under specific conditions — members with less than 10 years of service can withdraw via Form 10C. Beyond 10 years, benefits convert to a monthly pension rather than a withdrawal.

What is pensionable salary?

The average monthly basic pay + dearness allowance over the 60 months preceding exit from the pension fund, capped at the statutory wage ceiling unless the higher-pension option was exercised.

How is the EPS pension calculated?

Monthly Pension = (Pensionable Salary × Pensionable Service) ÷ 70. This formula is unchanged under EPS 2026.

What is the retirement age under EPS?

Full pension at 58, with an option for reduced early pension from age 50. Unchanged under EPS 2026.

Conclusion

EPS 2026 is best understood as a legal modernization, not a pension redesign — your formula, contributions, and entitlements carry over unchanged. The parts that matter operationally are the new 20-day settlement deadline with real financial teeth, the codified statutory basis for higher pension, and a specific number for orphan pension. None of it substitutes for accurate EPFO records, which remain the single biggest lever most members actually control.