Last updated 11 July 2026. Based on the Employees' Provident Funds Scheme, 2026, notified by the Ministry of Labour and Employment in the Gazette of India on 29 June 2026 — cross-checked against PIB releases and EPFO's own circulars. If your claim depends on a specific number here, verify it against your EPFO passbook or book a free EPF audit — individual eligibility can vary by service history.

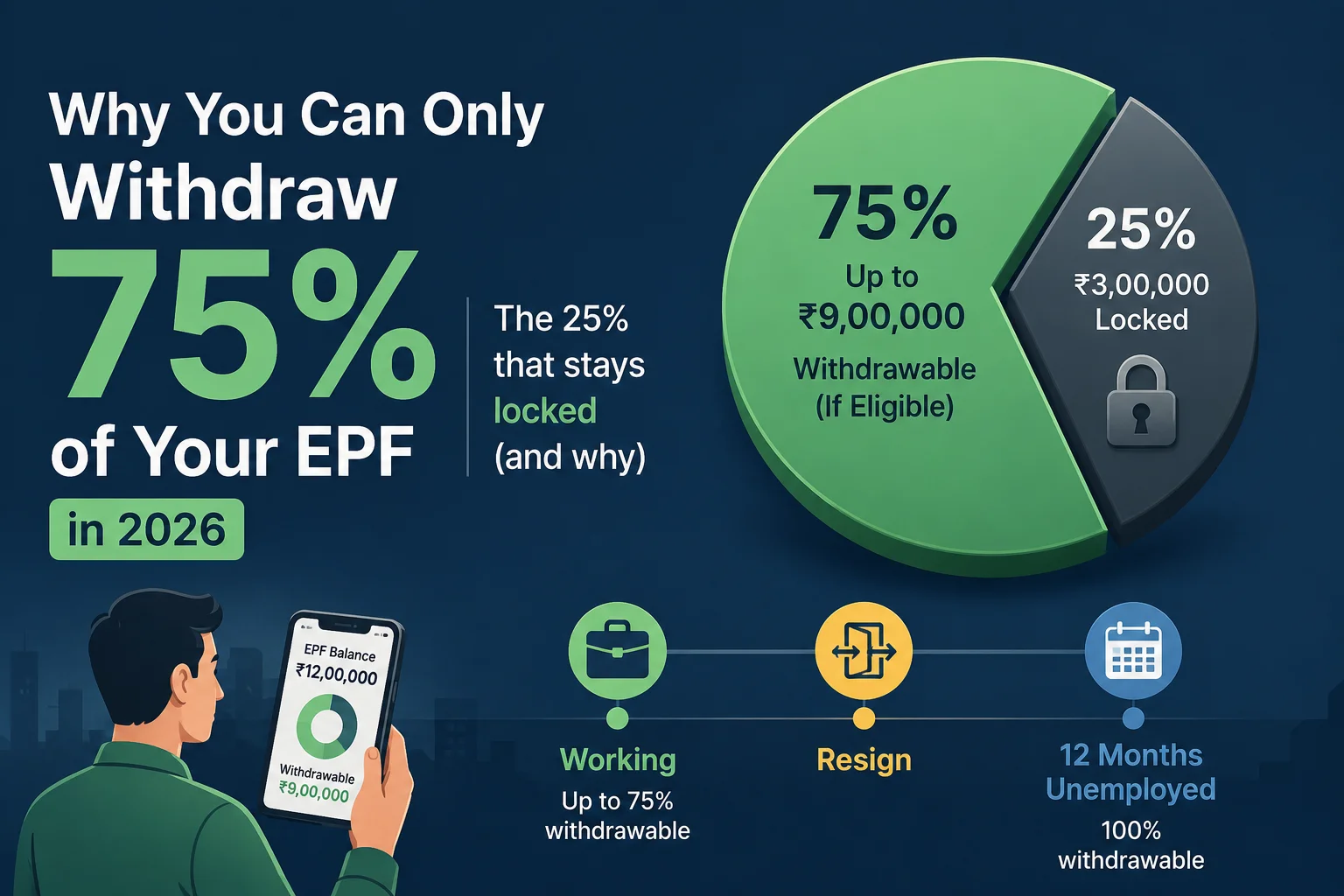

Short answer: You can withdraw 100% of your EPF only at final exit — retirement, 12 months of unemployment, permanent disability, retrenchment, VRS, or emigration. While still employed, the cap is 75% of your balance, category-restricted, and only after 12 months of EPF membership. The 25% floor cannot be touched until you formally exit.

If that contradicts something you read six months ago, you're not wrong — the rule changed under you.

The Two-Clock Rule

Every confusing case in this scheme resolves once you separate the two clocks that EPFO deliberately runs on different timers:

- Clock 1 — Membership clock: 12 months in the fund unlocks partial withdrawal (illness, education, marriage, housing) while you're still employed.

- Clock 2 — Unemployment clock: 12 months out of a job unlocks full withdrawal (100%, including the 25% floor).

They don't stack, and they don't share a start date. Someone with 8 years of membership who just lost their job still has to run Clock 2 in full — membership tenure doesn't shorten the unemployment wait.

What changed on 29 June 2026

The government notified the Employees' Provident Funds Scheme, 2026, replacing the 1952 scheme under the Code on Social Security, 2020. Existing balances, UANs, and past contributions carry over untouched — but the withdrawal framework was rebuilt.

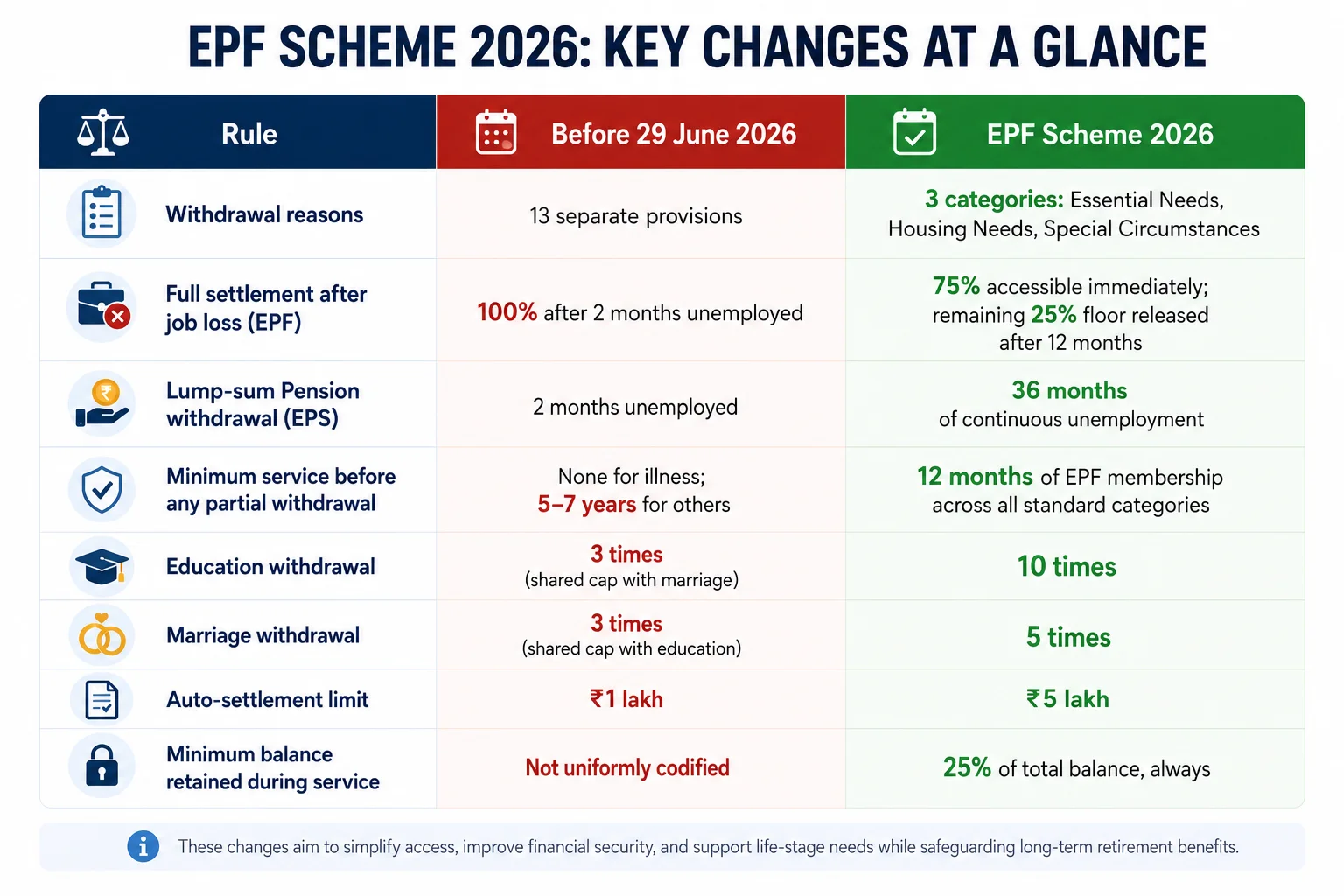

| Rule | Before 29 June 2026 | EPF Scheme 2026 |

|---|---|---|

| Withdrawal reasons | 13 separate provisions | 3 categories: Essential Needs, Housing Needs, Special Circumstances |

| Full settlement after job loss (EPF) | 100% after 2 months unemployed | 75% accessible immediately; remaining 25% floor released after 12 months |

| Lump-sum Pension withdrawal (EPS) | 2 months unemployed | 36 months of continuous unemployment |

| Minimum service before any partial withdrawal | None for illness; 5–7 years for others | 12 months of EPF membership across all standard categories |

| Education withdrawal | 3 times (shared cap with marriage) | 10 times |

| Marriage withdrawal | 3 times (shared cap with education) | 5 times |

| Auto-settlement limit | ₹1 lakh | ₹5 lakh |

| Minimum balance retained during service | Not uniformly codified | 25% of total balance, always |

The two changes that actually move the needle for most people: the unemployment wait for full settlement nearly tripled, and medical emergencies are no longer instant-access — both now sit behind a 12-month clock.

Which bucket are you in

| Your situation | What you can withdraw |

|---|---|

| Employed, under 12 months in the fund | Not yet eligible for any partial withdrawal |

| Employed, 12+ months in the fund | Up to 75% of the total balance, category-capped |

| Unemployed for under 12 months | Still not eligible for final settlement |

| Unemployed 12+ months | 100%, including the 25% floor |

| Retiring, disabled, retrenched, VRS, or emigrating | 100%, no waiting period |

Category-wise limits

| Category | Includes | Cap | Frequency |

|---|---|---|---|

| Essential Needs — Illness | Self or family medical treatment | Up to 100% of the eligible balance (≈75% of the total, since 25% stays locked) | No fixed limit |

| Essential Needs — Education | Self or children | Up to 100% of the eligible balance | 10 times |

| Essential Needs — Marriage | Self or family | Up to 100% of the eligible balance | 5 times |

| Housing Needs | Purchase, construction, home loan repayment, renovation | 75% of total funds | 5 times |

| Special Circumstances | CBT-notified emergencies | Case-specific | As notified |

All categories require 12 months of membership first. None of them let you touch the 25% floor while you're still employed.

Worked example

Priya has a total EPF balance of ₹12,00,000 (employee + employer share) and 3 years of membership.

- Still employed, withdrawing for her sister's wedding: Eligible balance = 75% of ₹12,00,000 = ₹9,00,000. She can claim up to this amount, capped further by any category-specific formula EPFO applies at filing. The remaining ₹3,00,000 (25%) stays locked.

- She resigns and stays unemployed for 12 months: She can now claim the full ₹12,00,000 — the 25% floor releases only at this point.

- She resigns and reapplies after 6 months unemployed: Still capped at 75% — Clock 2 hasn't completed, so the floor hasn't released yet.

Same person, same balance — the withdrawable amount changes only with which clock has run out.

Not sure where you land? Kustodian's EPF withdrawal calculator applies these rules to your actual balance and membership date.

Why can't you still touch 25% while working

EPF is built as a forced retirement corpus, not a savings account you can zero out on demand. The 25% floor exists to stop full liquidation during active service — it releases only at genuine exit (retirement, extended unemployment, disability, retrenchment, VRS, or emigration), never for a mid-career partial claim. The 2026 scheme keeps this rule and applies it more strictly than before.

Bottom line

- 100% only at final exit: retirement, 12-month unemployment, disability, retrenchment, VRS, or emigration.

- 75% cap during active service, after 12 months of membership, category-restricted.

- 25% floor never releases mid-career, regardless of how long you've been a member.

FAQ

Can I withdraw 100% of my PF while still employed?

No. The 75% cap and 25% floor apply throughout active service, regardless of category.

Has the 2-month unemployment rule been removed?

Yes, and it introduces a massive split between your accounts. For your main EPF (Provident Fund) balance, you can access 75% immediately after job loss, with the remaining 25% releasing at 12 months of continuous unemployment. However, if you want to withdraw your EPS (Pension) lump-sum amount, the waiting period has officially jumped to 36 months of unemployment.

Does the 12-month membership rule apply to medical emergencies?

Yes. Illness withdrawals no longer have a zero waiting period — 12 months of membership is now mandatory.

Is the 25% ever released before I leave my job?

No. It's released only at final exit — retirement, 12-month unemployment, disability, retrenchment, VRS, or emigration.

Do these new rules apply to claims I already filed?

No. They govern claims filed on or after 29 June 2026; earlier settled claims aren't reopened.

Does switching jobs count as unemployment?

No. If you move directly to a new employer, your EPF membership continues uninterrupted — Clock 2 never starts. Only a genuine gap without employment counts.

If I resign but join a new company after 4 months, do I lose eligibility?

You don't lose your balance or membership — it transfers. But since you were re-employed before completing 12 months unemployed, you were never eligible for final settlement during that gap; only partial withdrawal rules applied if you'd crossed 12 months of membership.

Can I withdraw from my second marriage or a second degree?

Yes, within the frequency caps — marriage up to 5 times, education up to 10 times, across your entire membership, not per event type.

What happens if I withdraw the full amount and then rejoin EPF later?

A fresh final settlement closes that account entirely. Rejoining EPF with a new employer creates a new membership record — your 12-month clocks restart.

Is the 75%/25% split based on my total balance or just my own contribution?

Total balance — employee share, employer share, and accrued interest combined. The 25% floor applies to the whole corpus, not just your contribution.

Does the new scheme change how EPF withdrawals are taxed?

No. Tax treatment is unchanged — withdrawals after 5 years of continuous service remain tax-free; earlier withdrawals above ₹50,000 attract TDS unless Form 15G/15H (or Form 121, effective April 2026) is filed.

Where can I confirm these numbers apply to my specific account?

Your EPFO passbook shows your membership start date and current balance. For a category-by-category eligibility check against your actual service history, use Kustodian's EPF withdrawal calculator or book a free EPF audit.

Bottom line

* 100% only at final exit: retirement (now lowered to age 55), 12-month unemployment, disability, retrenchment, VRS, or emigration.

* 75% cap during active service (after 12 months of membership), or immediately upon job loss.

* 25% floor stays locked until month 12 of continuous unemployment or formal final retirement exit.

* EPS Pension claims now carry a strict 36-month waiting period for full lump-sum withdrawal post-unemployment.

Not sure which category your service history actually qualifies you for, or whether your 12-month clock has started? Run your numbers through Kustodian's EPF withdrawal calculator or get a free EPF audit before you file.

Related reading:

- PF Balance vs Withdrawable Amount: What You Can Actually Take Out

- How to Withdraw EPF Online: UAN Portal & UMANG App Guide

- EPF Form 31: PF Advance Rules, Limits & Online Apply

- EPF Form 19: Eligibility, Rules & Tax (15G) Fixes

- NRI EPF Withdrawal: Rules, Tax & Online Claim Process

- EPFO Portal Update 2026: New Features Explained

This article is for informational purposes only and does not constitute legal or financial advice. EPFO rules and interpretations may be updated after this notification; always cross-check against the official Gazette notification or your EPFO circular before filing a claim. Written and reviewed by the Kustodian.life EPF & Compliance team, which has processed ₹200+ Cr in EPF, EDLI, and succession claims.

PF Interest Loss Calculator

See how much interest you lose every month your claim sits unresolved.