If an EPF member dies while covered, their family is entitled to a lump-sum payout under the Employees' Deposit Linked Insurance (EDLI) Scheme — automatically, at no cost to the employee, with no minimum service period in most cases. The payout is calculated from the member's wages and EPF balance, and falls between ₹2.5 lakh and ₹7 lakh.

That's the short version. The details that actually determine whether your family's claim goes through — resignation, job changes, missing nominees, employer defaults — are below, along with the exact formula EPFO uses to calculate the amount.

Not sure whether your family would actually receive the EDLI benefit? Understanding your eligibility, nominee details, and EPF records today can help avoid claim issues later. Read on to learn how EDLI works, who can claim, how the payout is calculated, and the common mistakes that can delay or reduce benefits.

Quick Answer

| Question | Answer |

|---|---|

| Who is covered? | Every EPF member, automatically, at establishments with 20+ employees |

| Minimum service required? | None for the standard benefit. A December 2025 EPFO update also guarantees a minimum payout for members who died before completing 12 months of continuous service (see below) |

| Payout range | ₹2.5 lakh (floor) to ₹7 lakh (cap) |

| Who receives it? | The registered nominee, or the eligible legal heir if there's no nomination |

| Cost to employee | Free — funded entirely by employer contribution |

Already confident you qualify? [[LINK: Start the EDLI claim process | EDLI Claim Process guide]]

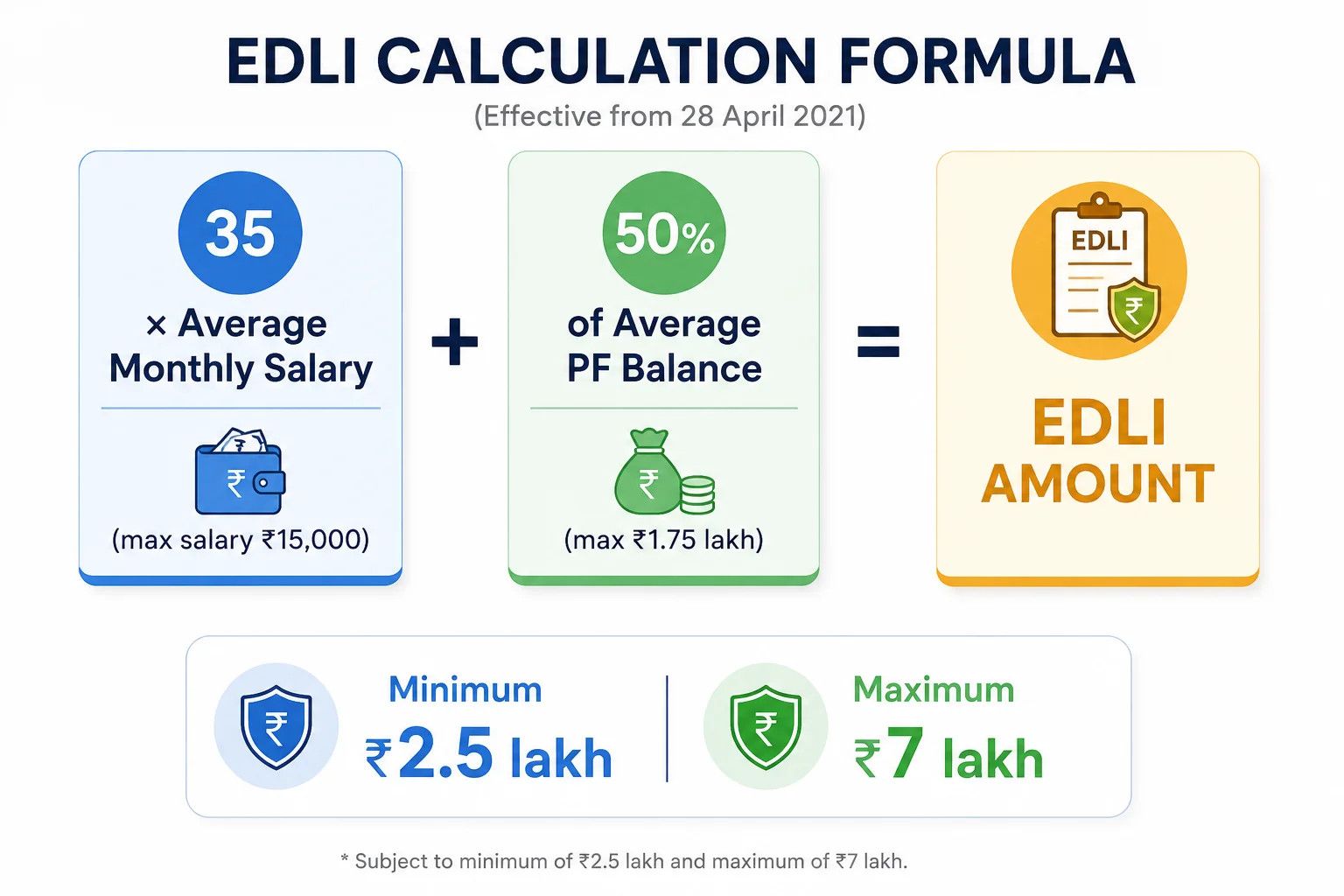

How Much Can You Actually Claim? (The Formula)

Most explainers stop at "up to ₹7 lakh." Here's how EPFO actually gets there, under the EDLI (Amendment) Scheme, 2021, effective 28 April 2021:

Benefit = (35 × average monthly wage over the last 12 months, wage capped at ₹15,000) + (50% of average EPF balance over the last 12 months, capped at ₹1.75 lakh) — subject to a floor of ₹2.5 lakh and a ceiling of ₹7 lakh.

Worked Examples

| Average Monthly Wage | Average PF Balance | Formula Result | Amount Payable |

|---|---|---|---|

| ₹5,000 | ₹20,000 | ₹1,75,000 + ₹10,000 = ₹1,85,000 | ₹2,50,000 (floor applies) |

| ₹10,000 | ₹80,000 | ₹3,50,000 + ₹40,000 = ₹3,90,000 | ₹3,90,000 |

| ₹15,000 | ₹3,00,000 | ₹5,25,000 + ₹1,50,000 = ₹6,75,000 | ₹6,75,000 |

| ₹15,000 | ₹5,00,000 | ₹5,25,000 + ₹1,75,000 (capped) = ₹7,00,000 | ₹7,00,000 (ceiling applies) |

Two things families consistently miss: even a low-wage, low-balance member's family gets at least ₹2.5 lakh — and going above ₹15,000 in wages doesn't increase the payout, since that portion of the formula is capped.

Eligibility Checklist

All four should be true for a standard claim:

| Requirement | Detail |

|---|---|

| EPF membership | Employee had an active EPF account at the time of death |

| Covered establishment | Employer has 20+ employees and is registered under the EPF Act |

| Death during eligible coverage | Employment/EDLI coverage was active, or fell within the extended grace periods below |

| Valid claimant | A registered nominee, or an eligible legal heir if no nomination exists |

If any of these is unclear in your case, [[LINK: get a free eligibility review | EDLI Eligibility Review CTA]] before you start collecting documents.

Who's Covered, by Employment Type

| Employee Type | Coverage |

|---|---|

| Private sector/factory employee | Covered automatically as an EPF member |

| Contract employee | Covered if EPF contributions were made through the employer or contractor — employment type doesn't disqualify you |

| Fixed-term employee | Covered on the same terms as permanent staff, as long as the EPF is applied |

| Part-time employee (multiple employers) | Wages from all EPF-covered employers are aggregated for the calculation, subject to the ₹15,000 wage cap |

| International worker | Covered under EPF's international worker provisions, or under a Social Security Agreement between India and the worker's home country, where applicable |

| Employee of an exempted PF trust | Still covered — the trust must meet its EDLI obligations either directly or through an approved equivalent scheme |

What Changed in December 2025: Continuous Service and Break-in-Service

This is the update most EDLI content online hasn't caught up to yet, and it directly affects two of the most common claim disputes: resignation and job-switching.

EPFO's December 2025 circular addressed cases where families were being denied EDLI benefits over technicalities:

- Minimum benefit for short service: Dependents of members who died without completing 12 months of continuous service, and whose average PF balance was under ₹50,000, are now guaranteed a minimum payout of ₹50,000 — previously, these cases could result in a much smaller or denied claim.

- Break-in-service fix: Weekends, holidays, and short gaps (up to 2 months) between leaving one EPF-covered job and joining another are no longer counted as a break in service. Several claims had been wrongly rejected because a Saturday–Sunday gap between employers was treated as a service interruption.

- Non-contributory period covered: Families of members who died within 6 months of their last EPF contribution — provided the member was still on the employer's rolls — are now eligible, even without a contribution in that final window.

If your case involves a recent job change, a short employment gap, or a death shortly after the last salary credit, this update likely works in your favor.

Not sure whether these updated EDLI rules apply to your case? Talk to a Kustodian expert for personalized guidance. We can help you understand your eligibility, review your EPF records, and navigate the EDLI claim process with confidence.

Common Scenarios

| Scenario | Eligibility |

|---|---|

| Died while actively employed and covered | Standard claim applies — proceed with Form 5(IF) |

| Died after resignation, before joining a new job | Not eligible once EPF/EDLI coverage has formally ended. If the resignation and death fall within the same short window covered by the December 2025 break-in-service update, the family may still qualify — check the exact dates against that rule |

| Died after retirement | Not eligible. EDLI covers death during active employment, not after retirement |

| Died during notice period | Eligible — an employee serving notice remains an EPF/EDLI member until employment officially ends |

| Died while on unpaid leave | Eligible if the employment relationship and EDLI coverage technically continued during the leave; check with the employer's HR/PF records |

| Died while switching jobs | Eligible in most cases post-December 2025, since short gaps between employers are no longer treated as a coverage break |

| The employer didn't deposit EPF contributions | Does not automatically disqualify the family. Liability for the employer's default sits with the employer — EPFO can still process the claim based on wage and service records |

Who Receives the Payout

A registered nominee receives the full amount; if there's no valid nomination, it goes to the eligible legal heir(s). If the nominee is a minor, the amount is paid to their legal guardian on their behalf.

Nomination disputes and multi-claimant situations have their own rules — see [[LINK: EDLI Nomination & Legal Heir Guide | Nomination guide]] for how to identify the correct claimant and what happens when there's no nomination on file.

Myths vs. Reality

| Myth | Reality |

|---|---|

| Only permanent employees qualify | Contract and fixed-term employees qualify too, if the EPF applies |

| You need years of service first | No minimum service is required for the standard benefit; short-service cases now have a ₹50,000 minimum under the Dec 2025 update |

| Only the spouse can claim | Any valid nominee or the eligible legal heir can claim |

| The employer decides if EDLI is payable | Eligibility is governed by EPFO rules — the employer has no discretion here |

| Resignation always kills eligibility | It usually does once coverage ends, but short gaps between jobs are now protected under the Dec 2025 circular |

Am I Eligible? (3-Step Check)

- Was the employee an active EPF member, or within a protected gap/grace period, at the time of death? If no, stop — not eligible. If yes, continue.

- Is there a registered nominee? If yes, they are the claimant. If no, the eligible legal heir is.

- Do you have the death certificate, service records, and claimant ID ready? If yes, you're ready to file.

Stuck on step 1 or 2? [[LINK: Talk to an EDLI expert | Expert review CTA]] — most cases can be confirmed in one conversation.

What to Do Next

| Next Step |

|---|

| File the claim |

| Gather documents |

| Complete the form |

| Confirm the right claimant |

| Claim already rejected or delayed |

FAQs

Is there a minimum service period for EDLI?

No, for the standard benefit. Members who die before completing 12 months of continuous service are now guaranteed a minimum of ₹50,000 under EPFO's December 2025 update, rather than being denied outright.

Can EDLI be claimed after resignation?

Only if EDLI coverage was still active at the time of death. A short gap between leaving one job and joining another is no longer automatically treated as a coverage break.

Can the family of a retired employee claim EDLI?

No — EDLI covers death during active employment, not after retirement.

Can contract or fixed-term employees receive EDLI?

Yes, if they were covered under EPF through their employer or contractor. Employment type doesn't affect eligibility.

What if the employer never deposited EPF contributions?

The family isn't automatically disqualified. The employer's default is a compliance issue on the employer's side; EPFO can still process the claim based on available records.

Can EDLI be claimed with no nominee on file?

Yes — the eligible legal heir(s) can claim, subject to standard documentation.

How is the EDLI amount calculated?

35 times the average monthly wage over the last 12 months (wage capped at ₹15,000), plus 50% of the average EPF balance over that period (capped at ₹1.75 lakh) — with a ₹2.5 lakh floor and ₹7 lakh ceiling.

Still have questions about your EDLI eligibility or claim? Every case is different, especially when it involves job changes, missing nominees, employer defaults, or incomplete EPF records. Talk to a Kustodian expert for personalized guidance on your situation and get help with documentation, eligibility checks, and the end-to-end EDLI claim process.

Sources

- Employees' Deposit-Linked Insurance (Amendment) Scheme, 2021 — Gazette notification, effective 28 April 2021

- EPFO circular on continuous service and break-in-service anomalies, December 2025

- Employees' Deposit Linked Insurance Scheme, 1976

- Employees' Provident Funds and Miscellaneous Provisions Act, 1952

This article explains the general EDLI framework and does not constitute legal advice. Individual claims depend on employment records and EPFO's assessment. [[LINK: Get a free case review | Eligibility Review CTA]] if your situation doesn't clearly match the scenarios above.

PF Interest Loss Calculator

See how much interest you lose every month your claim sits unresolved.