Facing a sudden job change, a career break, or a medical emergency can make your NPS savings feel like a lifeline you can't quite reach. The most common question for subscribers in this position is: “Can I take my NPS money out now, or is it locked until I’m 60?”

The short answer is yes, you can exit. However, unlike a simple savings account, a premature exit from the National Pension System (NPS) is a permanent decision that triggers specific regulatory guardrails.

In 2026, the landscape has shifted significantly to favor the subscriber. Following the latest PFRDA (Exits and Withdrawals) Amendment Regulations, the "small corpus" relief has been raised to ₹8 Lakh for normal exits and ₹5 Lakh for premature ones.

Furthermore, for the first time, non-government subscribers can withdraw up to 80% of their corpus as a lump sum. This guide walks you through these new 2026 regulations, the updated tax impacts, and how to avoid the "80% pension trap" to ensure you make the right move for both your current needs and your future security.

Contents

1. Troubleshooting NPS Withdrawal: "Why Is My Money Stuck?"

2. Defining "Final Exit" in the 2026 NPS Ecosystem

3. The "Small Corpus" Rule: How to Get 100% Cash

4. How the NPS Withdrawal Process Works in 2026

5. NPS Withdrawal Timelines: What to Expect in 2026

6. Top Reasons for NPS Withdrawal Delays & Failures

7. The 2026 Tax Trap: Is the 80% Lump Sum Tax-Free?

8. Knowing Who Is Responsible

9. When to Seek Expert Assistance for NPS Exits

10. Critical Mistakes to Avoid During Your Exit

11. Frequently Asked Questions

1. Troubleshooting NPS Withdrawal: "Why Is My Money Stuck?"

If you are reading this because your NPS withdrawal feels stuck, or because someone has told you that your money may not be released, it helps to begin with one clear point:

NPS withdrawal is a procedural right, not a discretionary decision.

If you meet the conditions prescribed under PFRDA regulations, your money cannot be refused. What can happen, and often does, is delay. These delays typically result from documentation gaps, verification mismatches, or coordination issues among multiple institutions involved in the exit process.

Is Your NPS Withdrawal Delayed or Stuck?

If your NPS withdrawal is delayed due to KYC issues, name mismatches, PRAN errors, documentation problems, or confusion around exit rules, you don't have to navigate the process alone.

Kustodian helps individuals resolve complex financial claim and withdrawal issues with expert guidance.

A Quick Status Check For NPS Before You Begin:

Your withdrawal options depend on why and when you are exiting NPS.

If You Are Retiring (Age 60 or Above)

At retirement, you have flexibility. You may:

- You can now withdraw up to 80% as a lump sum (up from 60%).

- Remain invested in NPS up to age 85, continuing market participation, and exit later

There is no obligation to exit exactly at 60.

If You Are Exiting Early (Below Age 60)

Under the All Citizen Model, there is no lock-in. You may exit at any time.

However:

- The mandatory annuity requirement is higher.

- The lump sum portion is restricted.

- Tax outcomes are different from retirement exits.

- The mandatory annuity requirement remains 80%, with only 20% as cash.

- The "Small Corpus" Rule (2026 Update): * Normal Exit (60+ or 15yrs):If your Tier-I corpus is ₹8 Lakh or less, you can withdraw 100% as a lump sum.Premature Exit: If your corpus is ₹5 Lakh or less, 100% withdrawal is allowed.

Early exit should therefore be a conscious decision, not a rushed one.

Get a thorough understanding NPS Premature Exit Rules 2026: Withdrawal & Tax Guide

If This Is a Death Claim

For most subscriber categories:

- The process is now largely online.

- Nominees can initiate the claim digitally.

- The entire corpus is payable to the nominee(s)

Annuity purchase is optional in most cases of death.

The Most Important Rule (Often Missed)

If your total Tier-I NPS corpus is ₹8 lakh or less at the time of exit:

- You are not required to purchase an annuity.

- You may withdraw the entire amount as a lump sum.

- The NPS account can be fully closed.

In practical terms, for smaller balances, NPS behaves much like a long-term investment product rather than a pension.

2. Defining "Final Exit" in the 2026 NPS Ecosystem

In everyday language, withdrawal sounds like a simple payout. In the NPS ecosystem, it means something very specific.

A withdrawal refers to a final exit from your Tier-I account.

Once you initiate “Final Exit,” the system begins a process that cannot be reversed midway.

Three things happen simultaneously.

PRAN Freeze

Your Permanent Retirement Account Number (PRAN) is frozen.

- No further contributions are allowed.

- The status change is permanent.

- Even if funds have not yet reached your bank, the exit cannot be cancelled

This is why it is important to verify bank details, KYC, and tax considerations before initiating the exit.

Corpus Segregation

Your total NPS balance is split into two parts:

- Lump sum portion, which is transferred to your bank account

- Annuity portion, which is sent to the chosen Annuity Service Provider

The exact split depends on:

- Your age

- Total corpus value

- Nature of exit (retirement, early exit, or death)

Multi-Institution Execution

Unlike mutual funds or bank deposits, NPS withdrawals involve multiple entities:

- The Central Record Keeping Agency (CRA) validates and authorises the request.

- The Trustee Bank releases the lump sum.

- The Annuity Service Provider (ASP) issues the pension policy

Each entity performs a specific role. Most delays occur between these handoffs, not because the request was rejected.

3. The "Small Corpus" Rule: How to Get 100% Cash

Rather than focusing on formulas, it helps to look at outcomes.

Below is a simplified, real-world view for non-government subscribers.

| Exit Scenario | Official Regulation | Total Corpus Limit | Max Lump Sum (Cash) | Annuity / SUR Requirement |

| Normal Exit (Age 60+ or 15 yrs) | Reg 4(1)(a) | ≤ ₹8 Lakh | 100% Cash | Annuity is Optional |

| Normal Exit (Mid-Range) | Reg 4(1)(a) | ₹8L – ₹12 Lakh | ₹6 Lakh | Balance via SUR (min. 6 yrs) or Annuity |

| Normal Exit (High Corpus) | Reg 4(1)(a) | > ₹12 Lakh | 80% Cash | 20% Mandatory Annuity |

| Premature Exit (Early) | Reg 4(b) | ≤ ₹5 Lakh | 100% Cash | Annuity is Optional |

| Premature Exit (High Corpus) | Reg 4(b) | > ₹5 Lakh | 20% Cash | 80% Mandatory Annuity |

Official Government Sources

Source https://www.pib.gov.in/PressReleasePage.aspx?PRID=2206763®=3&lang=2

Understanding Systematic Unit Redemption (SUR)

SUR allows subscribers to:

- Withdraw the lump sum gradually.

- Remain invested for up to six years.

- Avoid immediate annuity purchase for the entire balance.

This can help manage timing, taxation, and market exposure.

However, SUR availability depends on:

- CRA system enablement.

- Exit type.

- Subscriber eligibility.

It is permitted by regulation but may not be available in all cases at all times.

4. How the NPS Withdrawal Process Works in 2026

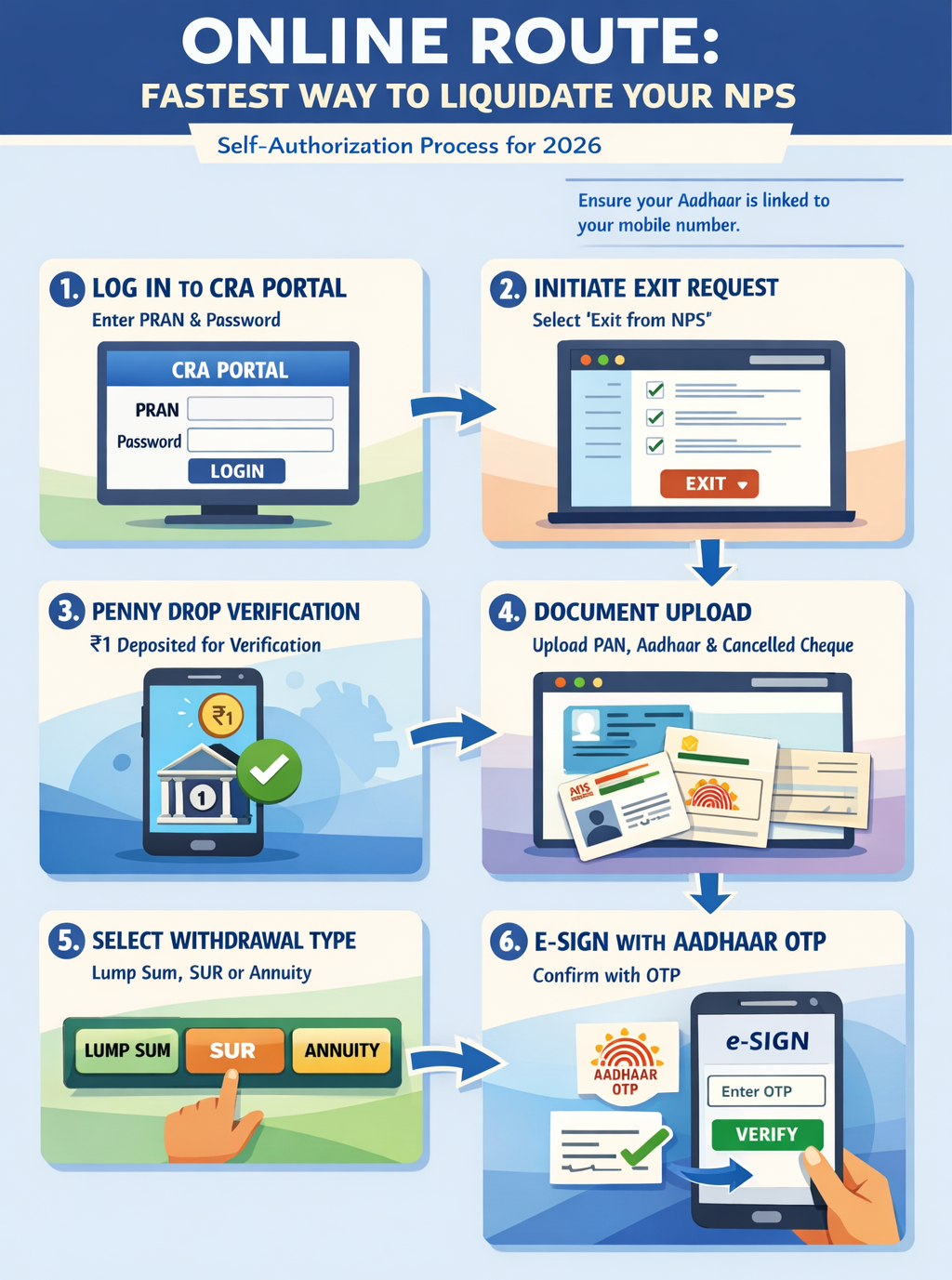

With the 2026 digital push, the Central Recordkeeping Agency (CRA) has streamlined the exit. You now have two primary pathways: the Self-Authorization (Online) route and the POP-Assisted (Offline) route.

The Online Route: Fastest Way to Liquidate

For most subscribers, this is a paperless, "Self-Authorization" journey. It is highly recommended that your Aadhaar be linked to your current mobile number.

- Step 1: Log in to CRA Portal (e.g., Protean or KFintech) using your PRAN and password.

- Step 2: Initiate Exit Request under the 'Exit from NPS' menu.

- Step 3: Penny Drop Verification – The system deposits ₹1 into your bank. In 2026, many banks use Pennyless API Verification, which instantly matches your name character-for-character with bank records.

- Step 4: Document Upload – Digitally upload your PAN, Aadhaar, and a cancelled cheque.

- Step 5: Select Withdrawal Type – Choose between Lump Sum, Systematic Unit Redemption (SUR), or Annuity.

- Step 6: e-Sign via Aadhaar OTP – This replaces physical signatures. Once confirmed, your PRAN is frozen.

The Offline Route: When Digital Fails

You must visit a Point of Presence (POP), usually your bank branch, if:

- Your Aadhaar-Mobile link is broken.

- "Penny Drop" Mismatch: Your bank name (e.g., A. Kumar) doesn't match your NPS name (Amit Kumar).

- The claim is a Death Claim (Nominees must submit physical forms).

- You are an NRI using an NRE/NRO account.

Switching from a Government job to Private? Your service history might be split. Ensure your tenure is correctly calculated by checking our Guide to EPF Service Transfers.

5. NPS Withdrawal Timelines: What to Expect in 2026

While the digital push has accelerated the "Final Exit" process, the NPS involves a chain of institutions. Here is the realistic T+ processing cycle (where T is the date of authorization):

| Stage of Exit | Entity Responsible | Expected Timeline |

| CRA Authorization | Central Record Keeping Agency | 1–2 Working Days |

| Lump Sum Credit | Trustee Bank (Axis/SBI/HDFC) | T+3 to T+5 Days |

| Annuity Policy Issuance | Annuity Service Provider (ASP) | 7–12 Working Days |

| First Pension Payout | Chosen Life Insurance Co. | Next Month Cycle |

6. Top 4 Reasons for NPS Withdrawal Delays & Failures

If your money is stuck, it is likely due to one of these four "Compliance Blockers." Under the 2026 PFRDA guidelines, these must be resolved before clicking submit:

- The "Penny Drop" Name Mismatch: If your name on the PRAN card is "Amit K. Sharma" but your bank account says "Amit Kumar Sharma," the verification will fail. You must update your NPS profile to match your bank records first.

- FATCA Non-Compliance: Mandatory for all subscribers, especially NRIs. If your FATCA self-certification is missing, the system will freeze the payout at the final stage.

- Dormant Bank Accounts: If you haven't used your linked bank account in over 12 months, the Trustee Bank's credit will bounce. Ensure your account is "Active" and has no credit limits.

- Frozen PRAN: If you missed the minimum annual contribution of ₹1,000 in previous years, your account might be "In-Active." You must unfreeze it by paying the penalty before initiating an exit.

Avoid the 80% Lock-in: Before you close your NPS account early, check if you can meet your immediate cash needs through an EPF advance instead. Learn the latest rules in our EPF Form 31: PF Advance & Loan Rules Guide.

Facing Repeated NPS Withdrawal Errors?

If your withdrawal request has been rejected, your claim is stuck in processing, or you're unsure which institution is causing the delay, getting expert guidance early can save weeks of follow-ups.

Kustodian assists individuals in resolving documentation issues, identifying procedural roadblocks, and navigating complex financial claims with confidence.

7. The 2026 Tax Trap: Is the 80% Lump Sum Tax-Free?

As of February 2026, there is a significant legal disconnect between PFRDA withdrawal rules (which allow you to take the money) and the Income Tax Act (which decides if you pay for it).

Lump Sum Exemption (Section 10(12A)

- The Conflict: The PFRDA (Exits and Withdrawals) Regulations, 2025, now permit you to withdraw up to 80% of your corpus as a lump sum. However, Section 10(12A) of the Income Tax Act explicitly exempts only 60% of the total corpus from tax.

- The Trap: Unless the Finance Act 2026 is amended by a special circular later this year, the "extra" 20% you withdraw will be added to your annual income and taxed at your applicable slab rate (e.g., 20% or 30%).

- The Strategy: If you don't need the full 80% immediately, stick to the 60% withdrawal to remain 100% tax-exempt.

Partial Withdrawal Exemption (Section 10(12B)

- The Rule: For medical emergencies, home buying, or higher education, you can withdraw up to 25% of your own contributions (not the total market-grown corpus).

- Tax Status: Under Section 10(12B), this amount is 100% Tax-Free. In 2026, the limit for these withdrawals has been increased to 4 times in a lifetime.

Annuity & Pension Taxation (Section 80CCD)

- Purchase Phase (Section 80CCD(5)): Any amount from your corpus used to purchase an annuity (minimum 20% required for large corpuses) is fully exempt from tax at the time of the transaction.

- Payout Phase (Section 80CCD(3)): This is the "deferred tax" part. The monthly pension you receive from your annuity provider is treated as "Income from Salary" or "Other Sources" and is fully taxable at your slab rate in the year you receive it.

Official Government Sources for Verification

To ensure your blog is seen as an authoritative "Expert" post (for GEO/SEO), link directly to these official portals:

- For Tax Sections: Income Tax Department (Official Statute) – Search for "Section 10(12A)" and "Section 10(12B)" in the Tax Law section.

- For Withdrawal Regulations: https://npstrust.org.in/sites/default/files/act-and-regulations-documents/GazettePFRDAExitandWithdrawalstheNPSAmendmentRegulations2025.pdf

For non-residents, the tax implications are even more complex due to DTAA rules. If you are an NRI, refer to our specific guide on NPS for NRI Taxation (2026) to avoid double taxation.

8. Knowing Who Is Responsible

Understanding accountability reduces frustration.

| Issue | Responsible Party |

| KYC or name mismatch | CRA |

| Amount debited but not credited | Trustee Bank |

| Pension not initiated | Annuity Service Provider |

Escalations work best when directed to the correct entity.

If you've already exhausted your NPS partial withdrawal limit, you might still be eligible for an EPF advance. Compare the two here: EPF vs. NPS: Which is better for emergencies?

9. When to Seek Expert Assistance for NPS Exits

Most users can navigate the portal independently. However, Professional Resolution is recommended in complex 2026 scenarios such as:

- NRE/NRO Repatriation: If you are an NRI trying to move NPS funds to an overseas account, the FEMA documentation can be grueling.

- Legacy Death Claims: Cases where the nominee is also deceased or the "Legal Heir" is not updated in the system.

- Multiple PRAN Mergers: If you accidentally held two PRANs during your career, you cannot exit one without merging both, a process that often requires manual intervention.

10. 4 Critical Mistakes to Avoid During Your Exit

- Premature Bank Closure: Never close your salary account until the NPS funds have hit the balance. Changing bank details after initiating an exit is a bureaucratic nightmare.

- Ignoring the "Small Corpus" Rule: If your balance is under ₹8 Lakh, don't accidentally opt for an annuity. You are entitled to the full 100% cash.

- Selecting the Wrong Annuity Variant: Once you choose "Annuity without Return of Capital," your principal is gone forever. Always double-check if you want the purchase price returned to your nominees.

- Market Timing Errors: Since NPS units are redeemed at the NAV of the day your request is processed, avoid initiating exits during extreme market volatility if you can wait.

11. Frequently Asked Questions

Q1: Can I really withdraw 80% as a lump sum? Is it tax-free?

Answer: While PFRDA regulations allow non-government subscribers to withdraw up to 80% of their corpus as a lump sum (leaving 20% for annuity), the tax rules may lag behind the withdrawal rules.

- The Trap: Currently, Section 10(12A) of the Income Tax Act explicitly exempts only 60% of the total corpus from tax.

- The Reality: If you withdraw 80%, the "extra" 20% might be added to your income and taxed at your slab rate unless the 2026 Finance Act specifically amends this exemption limit.

Q2: I got a "Penny Drop Failed" error during my exit. How do I fix it?

Answer: This is the #1 reason for withdrawal delays. It means the name in your NPS records does not exactly character-match the name in your bank account (e.g., "R. Kumar" vs. "Ramesh Kumar").

- The Fix: You cannot "force" the withdrawal. You must first update your name in your NPS records to match your bank passbook using Form S2 (or online profile modification). Once the names match, re-initiate the withdrawal request.

Q3: The portal says my claim is "Authorised," but I haven't received the money. Why?

Answer: "Authorised" means the CRA (Record Keeper) has cleared the paperwork. The actual funds move in two subsequent steps:

- Trustee Bank: Debits the funds (usually T+3 working days).

- Your Bank: Credits the account (usually T+4 or T+5 working days).

- Note: If 5 working days have passed since authorisation, check if your bank account is frozen, dormant, or inactive, as the transfer may have bounced.

Q4: My corpus is ₹7 Lakh. Do I have to buy an annuity (pension)?

Answer: No, if you are retiring (age 60+ or after 15 years), the new limit is ₹8 Lakh for 100% withdrawal. If you exit prematurely, you can only take 100% if the corpus is below ₹5 Lakh.

Warning for Early Exits: If you are exiting before age 60, this limit is lower (₹5 Lakh). Since ₹7 Lakh is above this early-exit limit, you would still be forced to purchase an annuity with 80% of the money if you quit early.

Q5: Can I surrender my annuity policy later and get my money back?

Answer: Generally, no. Once the annuity plan is purchased and the "Free Look Period" (usually 15-30 days after policy issuance) is over, the capital is locked for life. You cannot withdraw it for emergencies later. This is why choosing the right annuity option (e.g., Return of Purchase Price to Nominee) is critical at the time of exit.

Q6: I am a nominee filing a death claim. Can I take the whole amount?

Answer:

- If Corpus is ≤ ₹5 Lakh: Yes, you can withdraw 100% of the money.

- If Corpus is > ₹5 Lakh: You must use at least 80% (for Govt. Employees ) of the amount to buy an annuity (monthly pension) for the dependent spouse/mother/father. You can only withdraw 20% as cash.

- Exception: If there is no surviving spouse, mother, or father, the entire corpus may be paid to the surviving children/legal heirs without the annuity requirement.

- Q6: I am a nominee filing a death claim. Can I take the whole amount?

Closing Note: Navigating Your NPS Exit with Confidence

The 2026 NPS framework is designed for efficiency, but it remains a procedural and unforgiving system. While the digital transition has removed most human gatekeepers, it has replaced them with strict validation algorithms. If your documentation is seamless, the system works like clockwork; if there is a single character mismatch in your name or an inactive bank link, the process will halt without sentiment.

The Golden Rule for 2026: Do not treat an NPS withdrawal as a "request" that someone can approve or deny based on whim. Treat it as a financial transaction that requires 100% data accuracy.

Before you click that final "Submit" button, ensure your KYC is current, your FATCA is filed, and your Bank Account is active. Understanding these nuances today is the difference between receiving your funds in seven days or facing months of administrative follow-ups. Your retirement corpus is your hard-earned security. Exiting correctly is the final, and most important, step of that journey.

Need Help With Your NPS Withdrawal?

Whether you're retiring, exiting early, filing a nominee claim, or dealing with a delayed or rejected withdrawal, every situation is different. A small documentation mistake or eligibility issue can significantly delay your funds.

Kustodian helps individuals navigate complex financial claims and recover their rightful money with expert support.

✔ NPS withdrawal guidance

✔ EPF & pension claim assistance

✔ Financial asset recovery

✔ Estate and succession support

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.