Retirement planning is long-term, but life often demands short-term liquidity. Expenses like education, medical emergencies, or buying a home may require access to funds earlier than expected.

The National Pension System (NPS) allows this through partial withdrawal, a structured provision designed to provide limited access to savings without closing the account or affecting long-term retirement benefits.

Regulated by the Pension Fund Regulatory and Development Authority (PFRDA), NPS partial withdrawal lets eligible subscribers withdraw a portion of their own contributions for specific purposes. However, the rules are strict: withdrawal limits are contribution-based, permitted purposes are defined, and the number of withdrawals during a lifetime is capped. Understanding these conditions is essential to avoid claim rejection or unintended retirement impact.

Need help understanding whether you're eligible for an NPS partial withdrawal or how the rules apply to your situation? Our experts can guide you through the process and help you avoid common mistakes.

Contents

1. Navigating Financial Crisis: Why "Touch But Don’t Close" is the Best NPS Strategy for 2026

2. Deciphering the 2026 NPS Partial Withdrawal: Liquidity Without Losing Your Edge

3. Who is Eligible for NPS Partial Withdrawal in 2026?

4. Confirmed NPS Partial Withdrawal Rules (2026)

5. NPS Partial Withdrawal vs Premature Exit

6. Tax Treatment of NPS Partial Withdrawal: The 100% Tax-Free Advantage (2026)

7. How to Apply for NPS Partial Withdrawal in 2026

8. Why NPS Partial Withdrawal Requests Get Rejected

9. When Kustodian Life Can Help

10. Frequently Asked Questions

Closing Summary

1. Navigating Financial Crisis: Why "Touch But Don’t Close" is the Best NPS Strategy for 2026

For many NPS subscribers in India, reaching a point where you need urgent liquidity is common. Whether you are a corporate professional in Bengaluru, a government employee in Delhi, or an NRI managing an account from Dubai, life stages rarely wait for the perfect financial moment.

This realisation is often emotionally heavier than it appears on paper. Your PRAN (Permanent Retirement Account Number) isn't just a number; it represents a promise to your future self. Touching it can feel like breaking that discipline. However, a temporary cash crunch shouldn't lead to a permanent financial setback.

Common Liquidity Triggers in 2026:

- Education & Marriage: A child’s higher education at a premier Indian university or a wedding events that arrive at fixed stages.

- Medical Emergencies: Sudden hospitalisation requiring immediate funds, where waiting for insurance reimbursements isn't an option.

- First Home Purchase: Paying the down payment for a flat in a rising Indian real estate market (e.g., Mumbai, Pune, or Gurgaon) where timing is everything.

- Re-skilling: Funding a certification or skill development course to stay competitive in the evolving 2026 job market.

The Fear: "Will I Ruin My Retirement?"

The most common hesitation among Indian investors is the fear that accessing funds now will permanently damage their pension.

The reality is far more structured. Under the latest PFRDA (Pension Fund Regulatory and Development Authority) guidelines, an NPS partial withdrawal is not a loophole or a penalty; it is a designed liquidity feature. It allows you to address today’s obligations without sacrificing tomorrow’s security.

2. Deciphering the 2026 NPS Partial Withdrawal: Liquidity Without Losing Your Edge

An NPS partial withdrawal is often mistaken for an early exit, but the distinction is vital for your long-term wealth. In 2026, the PFRDA has refined these rules to ensure that a temporary financial crunch in cities like Mumbai or Delhi doesn't force you into a permanent retirement setback.

Think of it as a "Safety Valve." It provides immediate cash while keeping the engine of your retirement, the PRAN (Permanent Retirement Account Number), running at full speed.

Practical Impact: Your Wealth Stays on Track

When you opt for a partial withdrawal under the 2026 guidelines:

- Account Continuity: Your Tier-I account remains Active and continues to receive contributions.

- Compounding Uninterrupted: Only a portion of your own contributions is touched. The massive power of market-linked compounding on employer contributions and accumulated gains remains intact.

- Zero Penalties: Unlike breaking a Fixed Deposit (FD), there are no "premature" penalty rates, just structured access to your capital.

Simple Understanding: Partial Withdrawal vs. Premature Exit (2026)

| Feature | Partial Withdrawal | Premature Exit (Pre-60) |

| Primary Action | Accesses 25% of your principal. | Permanently closes the account. |

| PRAN Status | Remains Active. | Account is Terminated. |

| Liquidity Level | Limited to 25% of contributions. | 20% Lump sum (if corpus >₹5 Lakh). |

| The "Pension Trap" | No mandatory annuity. | 80% Locked in a monthly pension. |

| Verdict | Best for Life’s Milestones. | Last Resort (Total Exit). |

The 2026 Strategic Takeaway

If you are an Indian professional facing a high-cost event like a down payment for a property in Bengaluru’s tech corridor or funding a child’s overseas education, a Partial Withdrawal is the intended solution.

By avoiding a Premature Exit, you escape the "80% Trap," where the majority of your money gets locked into an annuity (pension) prematurely, often at lower returns than your active NPS market allocation.

Deep Dive: To understand the full implications of closing your account early and how to manage the mandatory annuity, read our detailed guide: NPS Premature Exit Rules 2026: New PFRDA Withdrawal Limits & Tax Impact.

3. Who is Eligible for NPS Partial Withdrawal in 2026?

Partial withdrawal in the National Pension System (NPS) is not an automatic right; it is a conditional benefit regulated by the PFRDA. Whether you are a central government employee in Delhi, a software professional in Hyderabad, or an NRI, eligibility is governed by specific structural milestones rather than just financial need.

To successfully unlock your funds in 2026, you must satisfy the following three-tier eligibility criteria:

Tier 1: The Tenure Milestone

You are only eligible to apply after completing a minimum of 3 years (36 months) as a subscriber.

- This is calculated from your date of joining (the date your PRAN was generated).

- Geo-Note: For those who have ported their account (e.g., moving from a Government job in West Bengal to a Corporate job in Karnataka), your total cumulative tenure is what counts.

Tier 2: Subscriber Category

The 2026 partial withdrawal facility is open to all major subscriber groups across India:

- Government Sector: Central and State Government employees.

- Corporate Sector: Employees of registered private companies.

- All Citizens Model: Self-employed individuals, professionals, and homemakers.

- NRIs/OCIs: Non-Resident Indians managing their accounts from abroad.

Tier 3: Account Status & Compliance

Your eligibility is often blocked by administrative status rather than tenure. Your request will only be processed if:

- Status is "Active": If you missed your minimum annual contribution, your account might be "Frozen" or "Inactive." You must regularize it before applying.

- Verified Bank Details: Under the 2026 verification rules, your PRAN name must match your bank records exactly to prevent fraud.

- KYC Compliance: Ensure your Aadhaar and PAN are linked and updated to avoid immediate rejection by the CRA (Central Recordkeeping Agency).

Critical Clarification: Intent vs. Structure

Eligibility is determined by structural compliance, not just the urgency of your reason. Even a critical medical emergency won't override the 3-year tenure rule.

If your NPS account is "Frozen" or "Inactive," you won't be able to initiate a withdrawal even if you've completed 3 years. This often happens due to missed annual contributions or outdated KYC. Check our Guide on Fixing Frozen NPS & PRAN Accounts to restore access before you apply.

4. Confirmed NPS Partial Withdrawal Rules (2026)

This is the section that determines whether your request will succeed or fail. Most rejections arise from misunderstanding these rules rather than from ineligibility.

4.1 How Much Can You Withdraw

You may withdraw up to 25% of your own contributions only.

What is included:

- Your personal contributions to NPS over time

What is excluded:

- Employer contributions

- Government contributions

- Market gains or investment growth

Example

Assume the following:

- Total personal contribution: ₹4,00,000

- Current market value of the account: ₹6,50,000

Even though the account is worth ₹6.5 lakh, the maximum eligible withdrawal is ₹1,00,000, calculated strictly as 25% of your own contributions.

Market gains are intentionally excluded to protect the long-term compounding objective of NPS.

Unsure how these rules apply to your NPS account?

Every withdrawal request is assessed based on PFRDA guidelines and your individual account details. If you need guidance before applying, we're here to help.

4.2 How Many Times Can You Withdraw

Partial withdrawal is allowed up to three times during the entire NPS tenure.

This limit is often misunderstood.

| Rule | Meaning |

| 4 withdrawals | Across your entire NPS journey |

| Not per year | No annual or periodic reset |

Each withdrawal permanently reduces your remaining allowed count.

Guardrail: Do not plan withdrawals assuming future relaxations or policy changes unless officially notified by PFRDA at the time of request.

New Rule: There is now a mandatory 4-year gap between two partial withdrawals (reduced from the previous 5-year requirement in some models). However, this gap is waived for medical emergencies.

4.3 Permitted Reasons

Partial withdrawal is allowed only for notified purposes. This is non-negotiable.

Allowed Reasons

- Children’s higher education

- Children’s marriage

- Purchase or construction of the first residential house (one-time only)

- Medical treatment or hospitalisation for:

- Skill development/re-skilling or any other self-development activities.

- Establishment of her/his own venture or any start-ups

[PFRDA rules do not allow withdrawal for general hospital emergencies (like a broken leg, dengue, or routine surgery). It is strictly restricted to a "Specified Critical Illness" list (e.g., Cancer, Kidney Failure, Stroke, Organ Transplant, Covid-19 with complications)].

Not Allowed

- Business or trading losses

- Personal loan repayment or credit card dues

- Lifestyle or discretionary spending (travel, gadgets, investments)

- General cash needs without documentary backing

Important: Selecting an incorrect purpose is one of the most common reasons for outright rejection.

NPS rules for buying a house are very strict (only allowed once and only if you don't own a property). If you need funds for home renovation or a second property, an EPF advance is far more flexible. Compare the two here: EPF Form 31: PF Advance Rules for 2026.

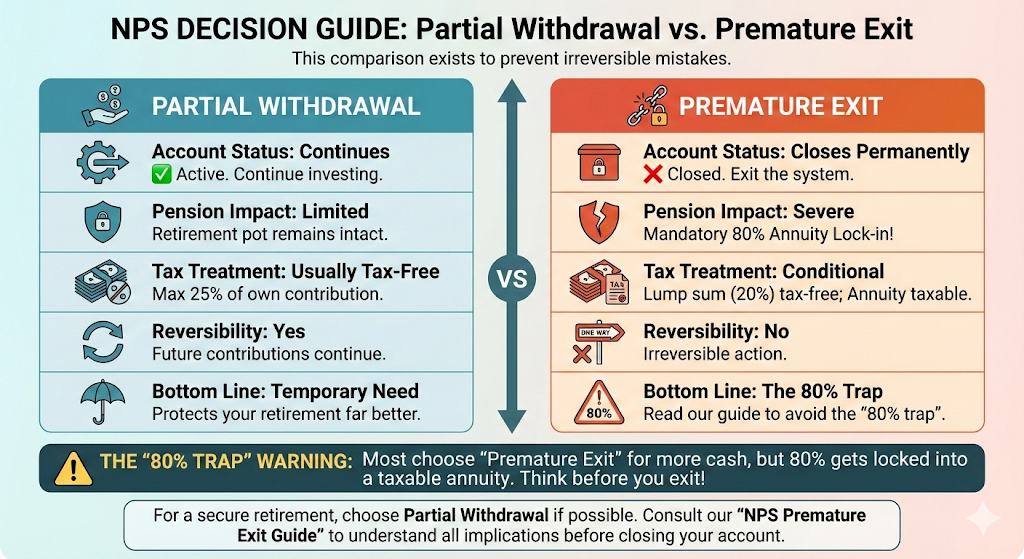

5. NPS Partial Withdrawal vs Premature Exit

This comparison exists to prevent irreversible mistakes.

| Aspect | Partial Withdrawal | Premature Exit |

| Account status | Continues | Closes permanently |

| Pension impact | Limited | Severe |

| Tax treatment | Usually tax-free | Conditional |

| Reversibility | Yes (future contributions continue) | No |

- Exit Flexibility:

- Full Withdrawal Thresholds:

("80/20 Rule" (80% Lump sum / 20% Annuity) for non-government employees at retirement.)

Bottom Line

If your financial need is temporary, a partial withdrawal protects your retirement far better than exiting NPS early.

Many people choose "Premature Exit" because they need more than 25% of their contribution. However, this triggers a mandatory 80% annuity lock-in. Before you close your account, read our NPS Premature Exit Guide to see if you can avoid the "80% trap."

6. Tax Treatment of NPS Partial Withdrawal: The 100% Tax-Free Advantage (2026)

This is the area that causes the most unnecessary hesitation among Indian investors. In the 2026 tax landscape, NPS partial withdrawal remains one of the most tax-efficient ways to access liquidity compared to traditional FDs or even some Mutual Funds.

Confirmed Rule (2026)

Under Section 10(12B) of the Income Tax Act, any partial withdrawal from your NPS Tier-I account is 100% Tax-Exempt, provided it meets the following PFRDA criteria:

- Limit: It is within 25% of your own contributions.

- Purpose: It is for one of the "notified purposes" (Education, Marriage, Housing, or Medical).

- Compliance: The withdrawal is executed through the official CRA portal (Protean/KFintech).

Debunking the Myths: 2026 Edition

| Common Myth | The 2026 Fact Check |

| "Partial withdrawal is added to my taxable income." | INCORRECT. Unlike an FD or certain EPF withdrawals, this amount is not added to your "Income from Other Sources." |

| "I have to pay capital gains tax on the growth." | INCORRECT. Since you only withdraw from your principal contribution, no capital gains tax is applicable at this stage. |

| "The 80% lump sum at retirement is also tax-free." | CAUTION. While PFRDA allows an 80% lump sum exit in 2026, the Income Tax Act currently only exempts up to 60%. The additional 20% may be taxed at your slab rate. |

Why It’s the "Safest" Liquidity Option in India

From a tax perspective, the NPS partial withdrawal is a superior choice for residents in high-tax brackets (30%+) because:

- No TDS: There is no Tax Deducted at Source (TDS) on partial withdrawals.

- Preserved Exemptions: Taking a partial withdrawal does not reverse the tax benefits you claimed in previous years under Section 80CCD(1B).

- Net Gain: You are effectively taking back "tax-saved" money without paying any tax on the way out.

While partial withdrawal is 100% tax-free, the extra 20% (between the 60% and 80% lump sum at retirement) is currently under debate; many experts suggest it may be taxed at slab rates unless specified in the 2026 Budget. To understand how to structure your final corpus to save lakhs in taxes, read our 2026 Guide on Retirement Taxation in India.

7. How to Apply for NPS Partial Withdrawal in 2026

The National Pension System has shifted toward a "Digital First" approach in 2026. The application process is now faster, often bypassing the need for physical paperwork if your Aadhaar is linked to your mobile number.

7.1 Modes of Application

- Online (Instant Processing):

- Offline (Through POP):

7.2 Timeline & Fund Credit

Under the T+2 settlement cycle active in 2026:

- Once authorized, the units are redeemed.

- The funds are typically credited to your bank account within 2 to 4 working days.

8. Why NPS Partial Withdrawal Requests Get Rejected

A rejection can be frustrating, especially during a crisis. In 2026, the PFRDA implemented "Enhanced Due Diligence," making the system safer but less forgiving of minor errors.

8.1 Top 5 Rejection Reasons in 2026

- Failure: This is the #1 cause of rejection. The system deposits ₹1 into your account to verify the name. If your name on the PRAN (e.g., Rajesh Kumar) doesn't match your bank records (R. Kumar), the request is automatically blocked.

- Missing FATCA Declaration: Particularly for NRIs and those who haven't updated their profile since 2024. Your account must be FATCA-compliant to process any payout.

- Cooling-off Period Violation: Trying to withdraw before the mandatory 4-year gap (unless for a waived medical reason).

- Inactive/Frozen Status: If your account is frozen due to pending KYC or missed minimum contributions, the withdrawal module will be disabled.

- Bank Account Eligibility: You must be the First Account Holder of the bank account linked to the PRAN. Joint accounts where you are the second holder will likely face rejection.

Facing an NPS Withdrawal Rejection?

If your NPS partial withdrawal request has been rejected and you're unsure why, don't ignore it. Many rejections are caused by documentation issues, KYC mismatches, or procedural errors that can often be resolved.

Useful Links & References

To help you explore the topic further and verify the official regulations governing NPS withdrawals, the following resources may be useful.

Official NPS & Regulatory Resources

• Pension Fund Regulatory and Development Authority (PFRDA)Official regulator of the National Pension System and issuer of all withdrawal guidelines.https://www.pfrda.org.in

• NPS Trust Oversight body responsible for safeguarding subscriber interests and ensuring compliance across the NPS ecosystem.https://npstrust.org.in

• Protean CRA (formerly NSDL e-Governance)Primary Central Recordkeeping Agency where most NPS subscribers manage their PRAN and submit withdrawal requests.https://cra-nsdl.com

• KFintech CRA PortalAlternative CRA platform used by many NPS subscribers to manage accounts and process withdrawals.https://nps.kfintech.com

• Income Tax Department – Section 10(12B)Official reference for the tax exemption applicable to NPS partial withdrawals.https://incometaxindia.gov.in

• NPS Subscriber Withdrawal Forms & Guidelines Official documentation issued by PFRDA for partial withdrawal, premature exit, and retirement exit processes.https://www.pfrda.org.in/index1.cshtml?lsid=85

9. When Kustodian Life Can Help

Assistance is usually useful when:

- A valid withdrawal request is repeatedly rejected.

- Urgent medical withdrawals face delays.

- Documentation disputes arise across institutions.

- Multiple withdrawals need careful planning without exhausting lifetime limits.

Our role is to help you access liquidity within the rules, without weakening the retirement foundation you have spent years building.

Is Your Withdrawal Stuck on "Pending"?

If you've submitted your request but haven't received the funds, it’s usually due to a "Penny Drop" failure or a name mismatch with your bank. Let our experts run a Free NPS Diagnostic Scan to pinpoint the exact technical blocker holding up your money.

10. Frequently Asked Questions

Is NPS partial withdrawal tax-free?

Yes. NPS partial withdrawal is tax-free when it is:

- Within the prescribed 25% limit of your own contributions, and

- For permitted purposes notified by PFRDA.If either condition is violated, the request itself is usually rejected rather than taxed.

Can I withdraw market gains through a partial withdrawal?

No. Only your own contributions are eligible. Employer/government contributions and market gains are excluded to protect long-term compounding.

Can I do a partial withdrawal after age 60?

Generally, no. Partial withdrawal applies during the accumulation phase. After age 60, withdrawals are governed by retirement exit rules, not partial-withdrawal provisions.

Does partial withdrawal reduce my pension?

Yes, but marginally. Since only a portion of your own contributions is withdrawn, the impact is far smaller than a premature exit, which permanently closes the account.

How many times can I withdraw from NPS?

Up to three times across your entire NPS tenure. This is a lifetime limit with no annual reset, so each withdrawal should be planned carefully.

Closing Summary

NPS partial withdrawal is a designed safety valve, not a loophole.

When used correctly, it provides timely liquidity without forcing irreversible retirement decisions. Most problems arise not from the rules themselves, but from misunderstanding or misapplication.

If your need is real but temporary, partial withdrawal allows you to meet today’s obligation without sacrificing tomorrow’s security.

Need Help with Your NPS Withdrawal?

Whether you're planning your first partial withdrawal, facing a rejected request, or unsure about your eligibility, getting the process right the first time can save you time and unnecessary delays.

At Kustodian, we help individuals understand NPS withdrawal rules, review documentation, identify the cause of claim issues, and guide them through the resolution process.

Related Deep Dives for You:

- For NRIs: [The NRI’s Guide to EPF Taxation, TDS & DTAA (2026)]

- On Reforms: [EPFO Rule Changes 2026: Complete Summary of New PF & Pension Reforms]

- On Security: [How to Find a Deceased Person’s Bank Accounts, Property & Unclaimed Assets in India (2026)]

- On Technical Fixes: [EPF Joint Declaration Form: Name, DOB & Detail Correction Guide

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and PFRDA processing.